---

title: "Validation and the Bias-Variance Tradeoff"

execute:

enabled: true

jupyter: python3

---

A hospital is considering an AI system that predicts which patients will develop sepsis — a life-threatening condition where early intervention is critical. The vendor, Epic Systems, reports an AUC of 0.76–0.83. The hospital buys the system and deploys it. What questions should they have asked?

When researchers at Michigan Medicine independently evaluated the model on 27,697 hospitalized patients, they found an AUC of just 0.63 — barely better than chance. The model missed 67% of sepsis cases while firing false alerts on 18% of all hospitalizations, drowning nurses in alarms for patients who were fine.^[Wong et al., "External Validation of a Widely Implemented Proprietary Sepsis Prediction Model in Hospitalized Patients," *JAMA Internal Medicine*, 2021. <https://pmc.ncbi.nlm.nih.gov/articles/PMC8218233/>] The root cause: Epic evaluated the model on data similar to its training data, not on an independent external test set. The model had learned patterns specific to one hospital system's patient population and coding practices. Those patterns didn't generalize.

The Epic sepsis model is not an isolated failure. Dermatology AI systems have reported 90%+ accuracy on light skin tones but as low as 17% on dark skin, because the test sets didn't reflect the diversity of the deployment population.^[Daneshjou et al., "Disparities in Dermatology AI Performance on a Diverse, Curated Clinical Image Set," *Science Advances*, 2022.] Amazon built an AI recruiting tool that achieved high accuracy but systematically penalized resumes containing the word "women's" — the model had learned to replicate historical hiring bias embedded in its training data, and the company scrapped it.^[Dastin, "Amazon scraps secret AI recruiting tool that showed bias against women," *Reuters*, 2018.] In each case, the model looked good on data it had already seen but failed on the data that mattered.

:::{.callout-important}

## Definition: Distribution Shift

**Distribution shift** occurs when the data a model encounters at deployment differs systematically from its training data. Common forms:

- **Covariate shift**: the input distribution changes (e.g., training on one hospital's patients, deploying at another with different demographics)

- **Temporal shift**: the world changes over time (e.g., consumer preferences, market conditions, pandemic disruptions)

- **Label shift**: the outcome distribution changes (e.g., disease prevalence differs between screening populations)

:::

Before trusting any model's reported performance, ask: training data from *when*? From *where*? From *whom*? Is the deployment population the same? The Epic sepsis model trained on one hospital system and deployed at another. The dermatology AI trained on light skin and deployed on everyone. In each case, the mismatch between training and deployment data — distribution shift — explains the failure.

In [Chapter 5](lec05-feature-engineering.qmd), we engineered features — dummies, polynomials, interactions — and saw that a linear model can capture surprisingly complex patterns. In [Chapter 6](lec06-trees.qmd), we met decision trees and random forests, which engineer features automatically. But we've been measuring performance on the *same data we trained on*. Evaluating a model on its training data is like grading a student on the questions they've already seen — of course they'll do well. The question the hospital *should* have asked is the question this chapter answers: **does this model generalize?** We'll develop the tools to answer it: train/test splits, cross-validation, and the bias-variance tradeoff that explains why more complex models don't always win.

:::{.callout-note}

## All Models Are Wrong

"All models are wrong, but some are useful." — George Box (1976)

Every model simplifies reality. The question is never *whether* a model is exactly right — no model is. The question is whether the model's approximation is close enough to be useful for the decision at hand. The entire machinery of validation exists to answer that question.

:::

```{python}

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

from sklearn.linear_model import LinearRegression, Lasso, LassoCV

from sklearn.preprocessing import PolynomialFeatures

from sklearn.model_selection import cross_val_score, train_test_split

from sklearn.metrics import r2_score, mean_squared_error

import warnings

warnings.filterwarnings('ignore')

sns.set_style('whitegrid')

plt.rcParams['figure.figsize'] = (7, 4.5)

plt.rcParams['font.size'] = 12

DATA_DIR = 'data'

```

## Adding features: diminishing returns

Adding features always improves training $R^2$. But does it improve predictions on *new* data — and if so, by how much?

Let's find out. We'll build feature matrices at six different complexity levels — from minimal (just bedrooms and bathrooms) to kitchen-sink (all pairwise interactions) — and track performance on both the training and test sets.

```{python}

# Load Airbnb data (same setup as Chapter 5)

listings = pd.read_csv(f'{DATA_DIR}/airbnb/listings.csv', low_memory=False)

cols = ['price', 'bedrooms', 'bathrooms', 'room_type', 'neighbourhood_group_cleansed']

df = listings[cols].dropna().copy()

df = df.rename(columns={'neighbourhood_group_cleansed': 'borough'})

# Convert price to numeric

df['price'] = pd.to_numeric(df['price'].astype(str).str.replace('[$,]', '', regex=True), errors='coerce')

# Filter to reasonable prices (drops ~15% of listings at the extremes)

n_before = len(df)

df = df[df['price'].between(10, 500)].reset_index(drop=True)

print(f"Filtered from {n_before:,} to {len(df):,} listings (${10}–${500} range)")

y = df['price']

print(f"{len(df):,} listings")

df.head()

```

Here's the plan: six levels of model complexity, each one adding to the previous.

| Level | What it adds | Intuition |

|-------|-------------|-----------|

| 1 | bedrooms + bathrooms | Raw numeric features only |

| 2 | + room type dummies | Different baseline by listing type |

| 3 | + borough dummies | Different baseline by location |

| 4 | + bedroom x borough interactions | Different slopes by location |

| 5 | + polynomial features (degree 3) | Nonlinear numeric effects |

| 6 | all pairwise interactions | Everything interacts with everything |

```{python}

def build_features(data, level):

"""Build feature matrices at different complexity levels."""

num = data[['bedrooms', 'bathrooms']].copy()

if level == 1:

return num

room = pd.get_dummies(data['room_type'], drop_first=True, prefix='room')

if level == 2:

return pd.concat([num, room], axis=1)

borough = pd.get_dummies(data['borough'], drop_first=True, prefix='boro')

if level == 3:

return pd.concat([num, room, borough], axis=1)

# Level 4: add bedroom x borough interactions

inter = borough.multiply(data['bedrooms'], axis=0)

inter.columns = [f'{c}_x_bed' for c in inter.columns]

if level == 4:

return pd.concat([num, room, borough, inter], axis=1)

# Level 5: add polynomial features (degree 3) on numeric columns

poly = PolynomialFeatures(degree=3, include_bias=False)

num_poly = pd.DataFrame(

poly.fit_transform(num),

columns=[f'poly_{i}' for i in range(poly.n_output_features_)],

index=data.index

)

if level == 5:

return pd.concat([num_poly, room, borough, inter], axis=1)

# Level 6: kitchen-sink — all pairwise interactions

base = pd.concat([num, room, borough], axis=1)

poly_all = PolynomialFeatures(degree=2, interaction_only=True, include_bias=False)

all_inter = pd.DataFrame(poly_all.fit_transform(base), index=data.index)

return all_inter

```

Now the critical step: **split the data before fitting any models.** We train on 70% and evaluate on the held-out 30%. The test set simulates "new data" we haven't seen.

```{python}

# Split into train and test FIRST — before looking at any results

np.random.seed(42)

train_idx, test_idx = train_test_split(range(len(df)), test_size=0.3, random_state=42)

df_train = df.iloc[train_idx].reset_index(drop=True)

df_test = df.iloc[test_idx].reset_index(drop=True)

y_train = df_train['price']

y_test = df_test['price']

print(f"Train: {len(df_train):,} | Test: {len(df_test):,}")

```

We fit a `LinearRegression` at each complexity level and record both training and test $R^2$.

```{python}

model_names = [

'1: bedrooms+bath',

'2: + room_type',

'3: + borough',

'4: + interactions',

'5: + polynomials',

'6: all pairwise'

]

train_r2s = []

test_r2s = []

n_features_list = []

for level in range(1, 7):

X_tr = build_features(df_train, level)

X_te = build_features(df_test, level)

m = LinearRegression().fit(X_tr, y_train)

train_r2s.append(m.score(X_tr, y_train))

test_r2s.append(r2_score(y_test, m.predict(X_te)))

n_features_list.append(X_tr.shape[1])

results_df = pd.DataFrame({

'Model': model_names,

'Features': n_features_list,

'Train R²': [f'{r:.4f}' for r in train_r2s],

'Test R²': [f'{r:.4f}' for r in test_r2s]

})

print(results_df.to_string(index=False))

```

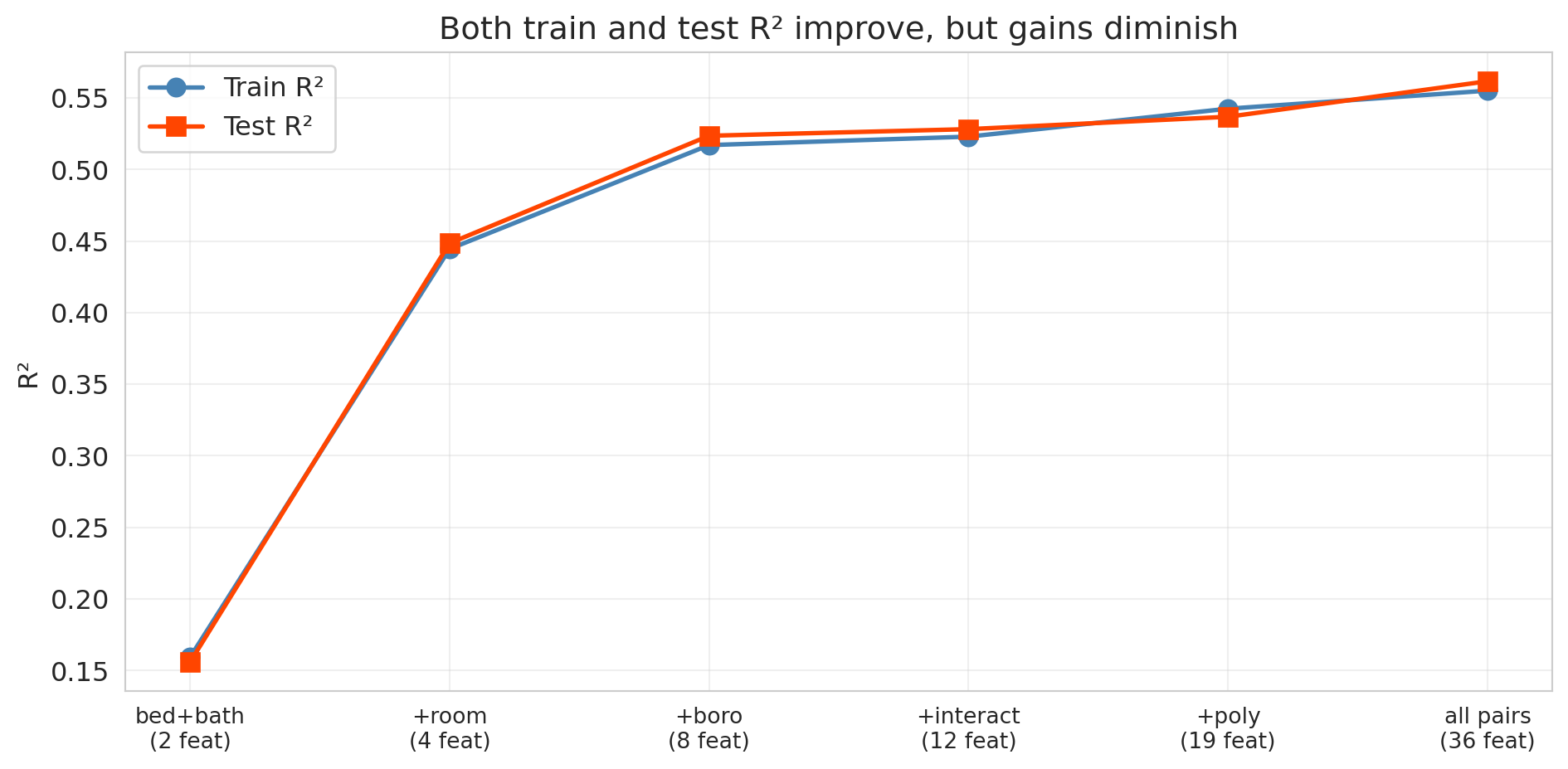

Training $R^2$ increases monotonically, as guaranteed. What about test $R^2$?

```{python}

fig, ax = plt.subplots(figsize=(10, 5))

x_pos = range(len(model_names))

ax.plot(x_pos, train_r2s, 'o-', color='steelblue', linewidth=2, markersize=8, label='Train R²')

ax.plot(x_pos, test_r2s, 's-', color='orangered', linewidth=2, markersize=8, label='Test R²')

ax.set_xticks(x_pos)

ax.set_xticklabels([f'{n}\n({nf} feat)' for n, nf in zip(

['bed+bath', '+room', '+boro', '+interact', '+poly', 'all pairs'],

n_features_list)], fontsize=10)

ax.set_ylabel('R²')

ax.set_title('Both train and test R² improve, but gains diminish')

ax.legend(fontsize=12)

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

```

Look at the gap between the blue line (train) and the red line (test). Both keep climbing — each new batch of features captures real signal. But notice the **diminishing returns**: the jump from Level 1 to Level 3 is enormous, while Levels 4 through 6 add only marginal improvement. The train-test gap also widens slightly as we add more features, hinting that the model is beginning to fit noise alongside signal. With enough data (we have over 20,000 listings here), that noise-fitting doesn't dominate — all six feature sets genuinely help. But what happens with a smaller dataset or far more features? That's where overfitting becomes dramatic.

:::{.callout-tip}

## Think About It

Why does the training $R^2$ always go up? Adding a feature can only help the model fit the training data better — in the worst case, the model sets that feature's coefficient to zero.

:::

### When more features = worse predictions

The six-level experiment didn't overfit because we had plenty of data relative to the number of features (36 features for over 20,000 listings). Let's see what happens when that ratio flips. We'll use a smaller sample (500 listings) and increase the polynomial degree from 1 to 7, creating thousands of features from only 300 training observations. With far more features than data points, the overfitting is dramatic.

```{python}

np.random.seed(42)

# Smaller sample — overfitting is more dramatic with less data

df_small = df.sample(500, random_state=42).reset_index(drop=True)

y_small = df_small['price']

train_i, test_i = train_test_split(range(len(df_small)), test_size=0.4, random_state=42)

# Base features: numeric + dummies

base_cat = pd.get_dummies(df_small[['room_type', 'borough']], drop_first=True)

X_base_small = pd.concat([df_small[['bedrooms', 'bathrooms']], base_cat], axis=1)

degrees = [1, 2, 3, 4, 5, 6, 7]

train_scores_poly = []

test_scores_poly = []

n_feat_poly = []

for deg in degrees:

poly = PolynomialFeatures(degree=deg, include_bias=False)

X_poly = pd.DataFrame(poly.fit_transform(X_base_small))

n_feat_poly.append(X_poly.shape[1])

X_tr = X_poly.iloc[train_i]

X_te = X_poly.iloc[test_i]

y_tr = y_small.iloc[train_i]

y_te = y_small.iloc[test_i]

m = LinearRegression().fit(X_tr, y_tr)

train_scores_poly.append(m.score(X_tr, y_tr))

test_r2 = r2_score(y_te, m.predict(X_te))

test_scores_poly.append(test_r2)

print(f"Degree {deg}: {X_poly.shape[1]:5d} features | "

f"Train R² = {train_scores_poly[-1]:.3f} | Test R² = {test_r2:.3f}")

```

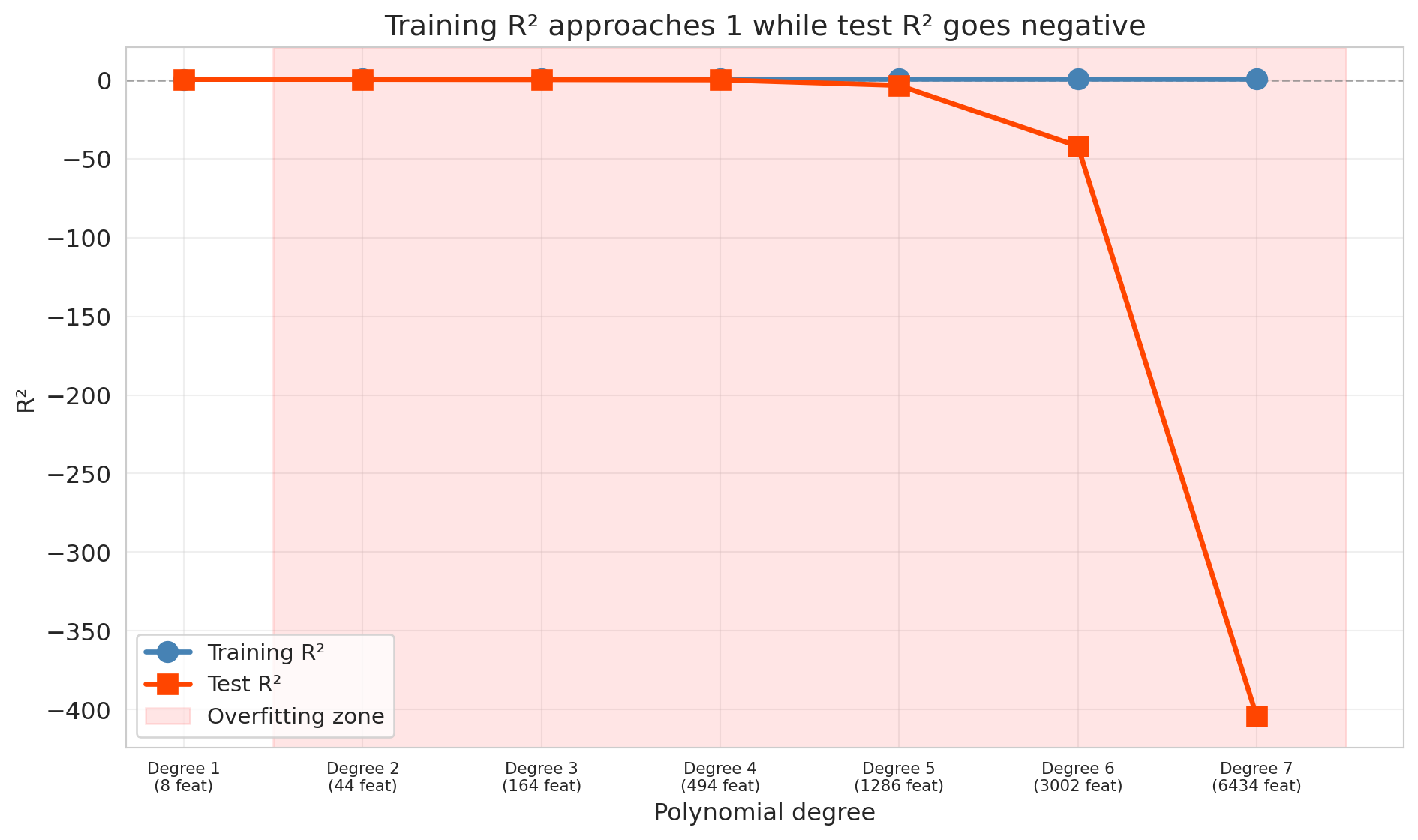

By degree 7, the model has over 6,000 features for only 300 training observations. The result is catastrophic overfitting.

```{python}

fig, ax = plt.subplots(figsize=(10, 6))

ax.plot(degrees, train_scores_poly, 'o-', color='steelblue', linewidth=2.5, markersize=10,

label='Training R²', zorder=3)

ax.plot(degrees, test_scores_poly, 's-', color='orangered', linewidth=2.5, markersize=10,

label='Test R²', zorder=3)

# Shade the overfitting region

best_test_idx = np.argmax(test_scores_poly)

if best_test_idx < len(degrees) - 1:

ax.axvspan(degrees[best_test_idx] + 0.5, degrees[-1] + 0.5, alpha=0.1, color='red',

label='Overfitting zone')

ax.axhline(y=0, color='gray', linestyle='--', linewidth=1, alpha=0.7)

ax.set_xlabel('Polynomial degree')

ax.set_ylabel('R²')

ax.set_title('Training R² approaches 1 while test R² goes negative')

ax.legend(fontsize=11)

ax.set_xticks(degrees)

ax.set_xticklabels([f'Degree {d}\n({n} feat)' for d, n in zip(degrees, n_feat_poly)],

fontsize=8)

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

```

The training $R^2$ approaches 1 — the model nearly perfectly memorizes the training data. Meanwhile, the test $R^2$ plummets, eventually going *negative*.

Wait — can $R^2$ be negative? Yes, on test data. On training data, $R^2$ is always between 0 and 1 (when the model includes an intercept). On test data, no such guarantee holds. Recall that $R^2 = 1 - \text{SS}_{\text{res}} / \text{SS}_{\text{tot}}$. When a model's predictions on new data are worse than simply predicting the mean every time, the residual sum of squares exceeds the total sum of squares, and $R^2$ drops below zero. Negative $R^2$ on test data means the model is worse than predicting the mean — a sign of catastrophic overfitting.

In [Chapter 6](lec06-trees.qmd), we saw similar overfitting with deep decision trees: a tree with no depth limit perfectly memorizes the training set but generalizes poorly.

## The bias-variance tradeoff

The polynomial experiment showed a striking pattern: test error first decreased and then increased as models got more complex. Why? The answer is one of the most important ideas in all of applied statistics: the **bias-variance tradeoff**.

:::{.callout-important}

## Definition: Bias and Variance

Two sources of prediction error:

- **Bias** is the error from oversimplifying. The model can't capture the true pattern. High bias corresponds to **underfitting** — like fitting a straight line through a curved relationship.

- **Variance** is the error from over-complicating. The model is so flexible that it's too sensitive to the particular training data it happened to see. High variance corresponds to **overfitting** — the model learns noise as if it were signal.

:::

| | Too few features | Just right | Too many features |

|---|---|---|---|

| **Bias** | High (underfitting) | Low | Low |

| **Variance** | Low | Low | High (overfitting) |

| **Test error** | High | **Low** | High |

For mean squared error, the decomposition is exact:

$$\text{Expected test error} = \text{Bias}^2 + \text{Variance} + \sigma^2$$

The first two terms depend on the model. The third term, $\sigma^2$, is the **irreducible noise** — inherent randomness in the outcome that no model can eliminate. Even a perfect model that recovers the true relationship still faces $\sigma^2$. Simple models have high bias but low variance. Complex models have low bias but high variance. The best model minimizes the sum of the first two terms; $\sigma^2$ sets the floor. A more advanced course will formalize this decomposition mathematically and use it to analyze regularization methods like lasso and ridge.

:::{.callout-tip}

## Think About It

In the polynomial experiment above, which degrees had high bias? Which had high variance? Where was the sweet spot?

:::

:::{.callout-note}

## Preview: regularization as bias-variance control

Another approach to controlling overfitting adds a **penalty** directly to the loss function. **Ridge regression** (L2 penalty) shrinks coefficients toward zero; **lasso** (L1 penalty) can shrink them exactly to zero, performing feature selection automatically. The bias-variance tradeoff governs the penalty strength: too little penalty and the model overfits (high variance); too much and it underfits (high bias). We introduce lasso later in this chapter.

:::

## Train, validation, and test sets

Before introducing cross-validation, we need to distinguish three roles that held-out data can play.

:::{.callout-important}

## Definition: The Three-Way Split

- **Training set** — the data the model learns from.

- **Validation set** — held-out data used to *choose* model complexity (number of features, regularization strength, tree depth). The modeler sees validation scores and adjusts accordingly.

- **Test set** — held-out data touched *only once*, at the very end, to report final performance. No modeling decisions depend on the test set.

:::

Why not just two sets? If we use the test set to choose among models, we are implicitly fitting to the test set. The reported "test" performance becomes optimistic — it no longer estimates how the model will perform on truly unseen data. A dedicated validation set absorbs the cost of model selection so the test set remains pristine.

In practice, a common split is 60% train / 20% validation / 20% test. Our earlier 70/30 split conflated validation and test — acceptable for a first look, but not for rigorous deployment. Cross-validation, introduced next, offers a more data-efficient alternative to a fixed validation set.

## Cross-validation

A single train/test split is noisy — we might get lucky or unlucky. Maybe our test set happened to contain easy-to-predict listings, or maybe the opposite. How do we get a more stable estimate of out-of-sample performance?

**Cross-validation** (CV) solves this problem by systematically rotating which data serves as the test set.

### How 5-fold CV works

1. Split the data randomly into 5 equal-sized **folds**

2. For each fold $k = 1, \ldots, 5$:

- Train the model on the other 4 folds

- Test on fold $k$ and record the score

3. Report the average of the 5 test scores

```

Fold 1: [TEST ] [train] [train] [train] [train] → score_1

Fold 2: [train] [TEST ] [train] [train] [train] → score_2

Fold 3: [train] [train] [TEST ] [train] [train] → score_3

Fold 4: [train] [train] [train] [TEST ] [train] → score_4

Fold 5: [train] [train] [train] [train] [TEST ] → score_5

Average → CV score

```

Every observation is in the test set exactly once. The average of 5 scores is much more stable than any single train/test split. (The extreme case is **leave-one-out CV** (LOO-CV), where $k = n$ — every observation gets its own fold. LOO-CV has low bias but high variance across folds, and is computationally expensive for large datasets. Five or ten folds is the usual practical choice.)

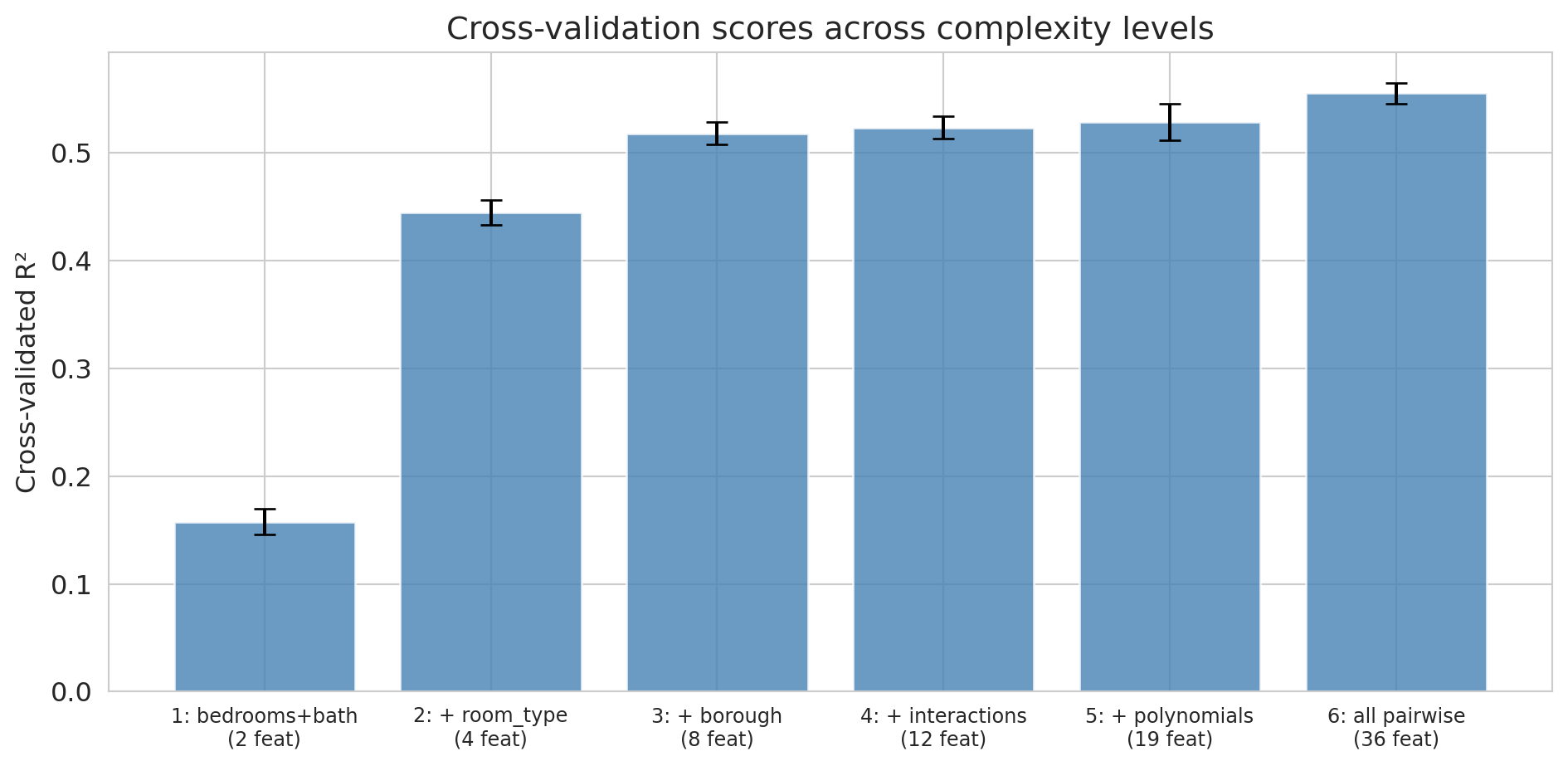

Let's apply 5-fold CV to our six complexity levels:

```{python}

cv_results = []

for level in range(1, 7):

X_all = build_features(df, level)

scores = cross_val_score(LinearRegression(), X_all, y, cv=5, scoring='r2')

cv_results.append({

'model': model_names[level-1],

'features': X_all.shape[1],

'cv_mean': scores.mean(),

'cv_std': scores.std()

})

print(f"Level {level}: CV R² = {scores.mean():.4f} ± {scores.std():.4f} ({X_all.shape[1]} features)")

cv_df = pd.DataFrame(cv_results)

```

The CV scores give us a more stable comparison than a single train/test split. Let's visualize them with error bars showing the standard deviation across folds.

```{python}

fig, ax = plt.subplots(figsize=(10, 5))

ax.bar(range(len(cv_df)), cv_df['cv_mean'], yerr=cv_df['cv_std'],

capsize=5, color='steelblue', alpha=0.8, edgecolor='white')

ax.set_xticks(range(len(cv_df)))

ax.set_xticklabels([f'{r["model"]}\n({r["features"]} feat)' for _, r in cv_df.iterrows()],

fontsize=9)

ax.set_ylabel('Cross-validated R²')

ax.set_title('Cross-validation scores across complexity levels')

plt.tight_layout()

plt.show()

best = cv_df.loc[cv_df['cv_mean'].idxmax()]

print(f"\nBest model by CV: {best['model']} (CV R² = {best['cv_mean']:.4f})")

```

Cross-validation confirms what the train/test split showed: all six feature sets genuinely help, and the most complex model (Level 6) has the best CV score. With plenty of data relative to the number of features, there's no overfitting to penalize here. Notice that the error bars (standard deviations across folds) give us a sense of how much variability there is — Levels 4 through 6 have overlapping error bars, so the gains from interactions and polynomials are modest. The polynomial experiment above is where CV would earn its keep: it would flag the point where additional polynomial terms start hurting.

:::{.callout-warning}

## CV Assumes Exchangeable Data

CV relies on the assumption that we can shuffle the data randomly — each fold is representative of the whole. The assumption breaks if the data have temporal structure. You can't train on 2024 data and "test" on 2023 data — the model would be peeking into the future. We'll see time-series validation in [Chapter 16](lec16-backtesting.qmd).

:::

## Lasso (regularization)

We've seen two strategies for handling overfitting:

1. **Manually choose** the right number of features using cross-validation

2. But what if we have hundreds of candidate features and don't know which ones matter?

There's a more elegant approach: let the model *automatically* shrink or eliminate unimportant features. That's **Lasso** (Least Absolute Shrinkage and Selection Operator), which adds an L1 penalty to the regression objective:

$$\min_\beta \sum_{i=1}^n (y_i - x_i^T \beta)^2 + \alpha \sum_{j=1}^p |\beta_j|$$

The penalty term $\alpha \sum |\beta_j|$ punishes large coefficients. The key property of L1: it drives some coefficients to *exactly zero*, effectively selecting features automatically.

A close relative is **ridge regression** (L2 regularization), which penalizes $\alpha \sum \beta_j^2$ instead. Ridge shrinks all coefficients toward zero but never sets them exactly to zero — it keeps all features but dampens them. The choice between lasso and ridge depends on whether you believe many features contribute small effects (ridge) or only a few features matter (lasso).

**Practical motivation:** Imagine you're building a medical screening tool. A model that requires 200 blood tests is impractical — it's expensive, slow, and fatiguing for patients. A model that needs 5 blood tests can actually be deployed in a clinic. Lasso finds the parsimonious model automatically.

```{python}

# Small sample to demonstrate overfitting vs. regularization

np.random.seed(42)

df_small = df.sample(500, random_state=42).reset_index(drop=True)

y_small = df_small['price']

train_i, test_i = train_test_split(range(len(df_small)), test_size=0.4, random_state=42)

base_cat = pd.get_dummies(df_small[['room_type', 'borough']], drop_first=True)

X_base_small = pd.concat([df_small[['bedrooms', 'bathrooms']], base_cat], axis=1)

# Use the kitchen-sink polynomial features (degree 3) on the small sample

poly_ks = PolynomialFeatures(degree=3, include_bias=False)

X_ks_small = pd.DataFrame(poly_ks.fit_transform(X_base_small))

X_ks_tr = X_ks_small.iloc[train_i]

X_ks_te = X_ks_small.iloc[test_i]

y_tr = y_small.iloc[train_i]

y_te = y_small.iloc[test_i]

# OLS on the same features (for comparison)

ols_ks = LinearRegression().fit(X_ks_tr, y_tr)

# Lasso automatically shrinks/eliminates features

lasso = Lasso(alpha=1.0, random_state=42).fit(X_ks_tr, y_tr)

n_total = X_ks_small.shape[1]

n_nonzero = (lasso.coef_ != 0).sum()

print(f"Kitchen-sink features: {n_total}")

print(f"Lasso keeps: {n_nonzero} features (zeroed out {n_total - n_nonzero})")

print()

print(f"OLS — Train R²: {ols_ks.score(X_ks_tr, y_tr):.3f} Test R²: {r2_score(y_te, ols_ks.predict(X_ks_te)):.3f}")

print(f"Lasso — Train R²: {lasso.score(X_ks_tr, y_tr):.3f} Test R²: {r2_score(y_te, lasso.predict(X_ks_te)):.3f}")

```

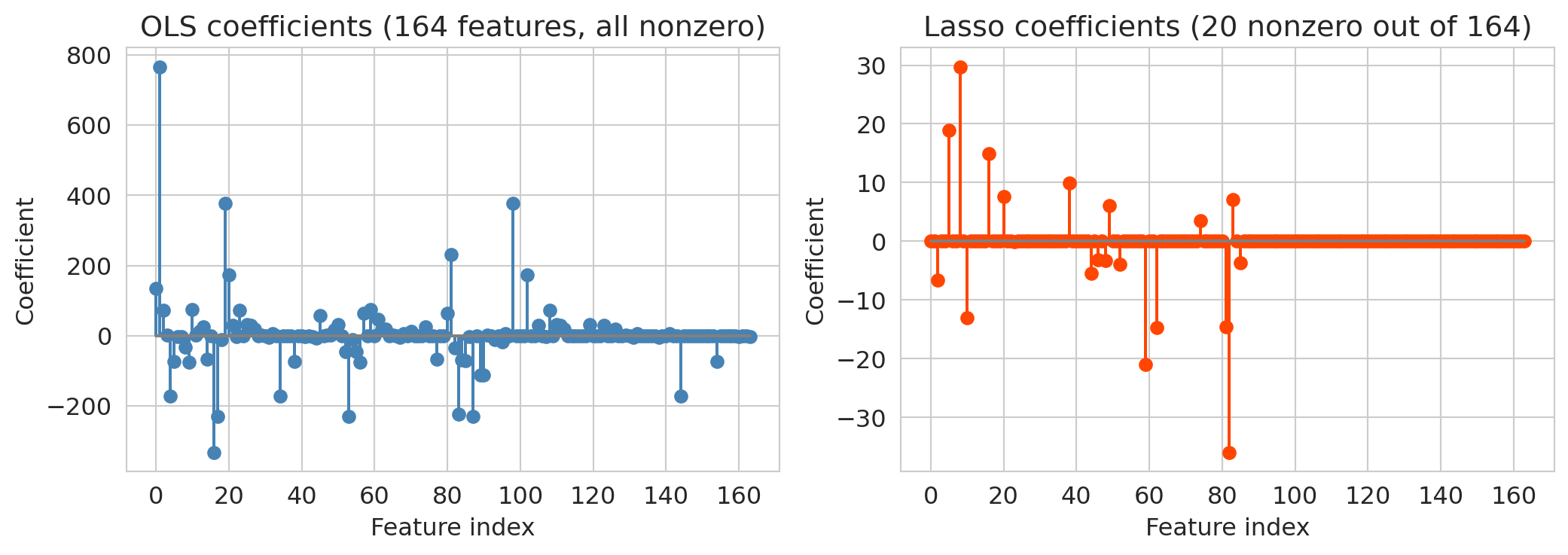

Lasso's test $R^2$ dramatically exceeds OLS on the same features. The coefficient plots below show why: OLS spreads weight across all features (many of which are noise), while `Lasso` zeros most of them out.

```{python}

# Visualize: Lasso coefficients vs OLS coefficients

fig, axes = plt.subplots(1, 2, figsize=(11, 4))

axes[0].stem(range(len(ols_ks.coef_)), ols_ks.coef_, linefmt='steelblue', markerfmt='o', basefmt='gray')

axes[0].set_title(f'OLS coefficients ({n_total} features, all nonzero)')

axes[0].set_xlabel('Feature index')

axes[0].set_ylabel('Coefficient')

axes[1].stem(range(len(lasso.coef_)), lasso.coef_, linefmt='orangered', markerfmt='o', basefmt='gray')

axes[1].set_title(f'Lasso coefficients ({n_nonzero} nonzero out of {n_total})')

axes[1].set_xlabel('Feature index')

axes[1].set_ylabel('Coefficient')

plt.tight_layout()

plt.show()

```

OLS uses all features and overfits more than Lasso — its test $R^2$ (~0.34) is notably worse than Lasso's (~0.48). Lasso aggressively zeros out the noise, keeping only the features that genuinely help prediction. It resolves the overfitting problem automatically: instead of manually choosing how many features to include, let the regularization penalty figure it out.

:::{.callout-tip}

## Think About It

The Lasso penalty strength $\alpha$ controls the bias-variance tradeoff. Large $\alpha$ = more regularization = more features zeroed out = simpler model (higher bias, lower variance). Small $\alpha$ = less regularization = closer to OLS (lower bias, higher variance). You can choose $\alpha$ by cross-validation — as we do next.

:::

### Choosing $\alpha$ by cross-validation

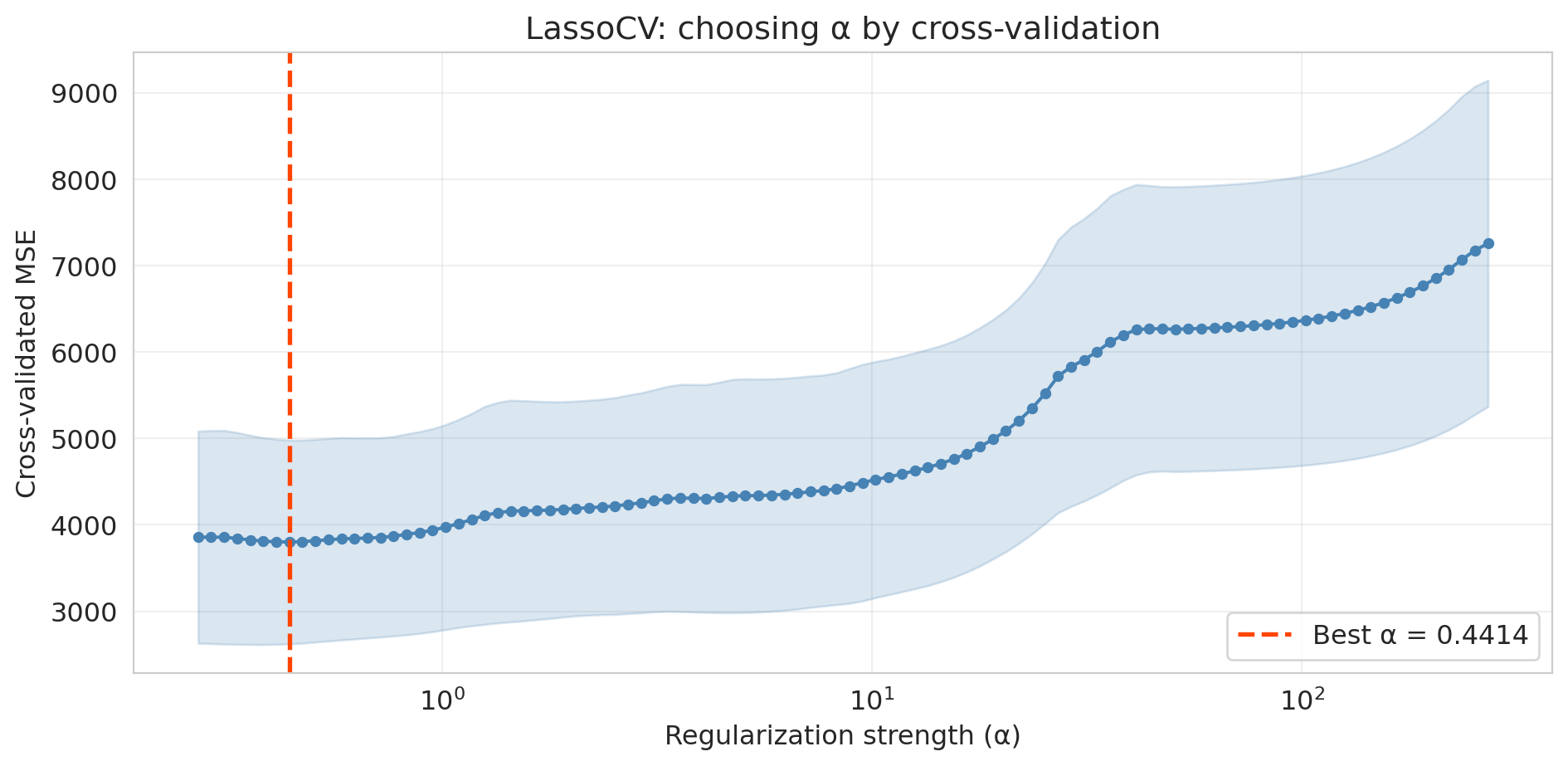

How do we pick the right $\alpha$? Scikit-learn's `LassoCV` automates the search: it fits lasso at many $\alpha$ values, scores each by cross-validation, and selects the $\alpha$ with the best CV performance.

```{python}

# LassoCV searches over a grid of alpha values using 5-fold CV

lasso_cv = LassoCV(cv=5, random_state=42, max_iter=10000).fit(X_ks_tr, y_tr)

print(f"Best alpha: {lasso_cv.alpha_:.4f}")

print(f"Nonzero coefficients: {(lasso_cv.coef_ != 0).sum()} out of {len(lasso_cv.coef_)}")

print(f"Train R²: {lasso_cv.score(X_ks_tr, y_tr):.3f}")

print(f"Test R²: {r2_score(y_te, lasso_cv.predict(X_ks_te)):.3f}")

```

```{python}

# Plot CV error as a function of alpha

fig, ax = plt.subplots(figsize=(10, 5))

# LassoCV stores the mean and std of MSE across folds for each alpha

alphas = lasso_cv.alphas_

mse_mean = lasso_cv.mse_path_.mean(axis=1)

mse_std = lasso_cv.mse_path_.std(axis=1)

ax.plot(alphas, mse_mean, 'o-', color='steelblue', markersize=4)

ax.fill_between(alphas, mse_mean - mse_std, mse_mean + mse_std, alpha=0.2, color='steelblue')

ax.axvline(lasso_cv.alpha_, color='orangered', linestyle='--', linewidth=2,

label=f'Best α = {lasso_cv.alpha_:.4f}')

ax.set_xscale('log')

ax.set_xlabel('Regularization strength (α)')

ax.set_ylabel('Cross-validated MSE')

ax.set_title('LassoCV: choosing α by cross-validation')

ax.legend(fontsize=12)

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

```

The U-shaped CV curve confirms the bias-variance tradeoff in action. Too small an $\alpha$ (right side) gives insufficient regularization — the model overfits. Too large an $\alpha$ (left side) penalizes too aggressively — the model underfits. `LassoCV` finds the valley automatically.

## The modern view: when more complexity helps

The classical bias-variance tradeoff says: more complexity eventually hurts. But in [Chapter 6](lec06-trees.qmd), we saw that random forests — averages of many overfit trees — improve with more trees, not fewer. That pattern departs from the U-shaped curve above.

The resolution: averaging independent overfit models (bagging) reduces variance without increasing bias. Each individual tree is high-variance, but their average is stable. The ensemble principle — that averaging independent overfit models can escape the classical tradeoff — motivates much of modern machine learning. (We demonstrated the effect in [Chapter 6](lec06-trees.qmd): adding more trees to a random forest reduced test error monotonically, with no U-shape.)

## Key takeaways

- **Evaluating on training data overstates performance.** Training $R^2$ measures memory, not understanding. A model that memorizes training data can fail on new data.

- **Train/test split gives honest error estimates.** Holding out data the model never sees during training simulates deployment conditions.

- **Cross-validation averages over multiple splits for stability.** CV rotates which fold is held out and averages the results, giving a reliable estimate of out-of-sample performance.

- **Bias-variance tradeoff: simple models underfit, complex models overfit.** Expected test error = bias$^2$ + variance + $\sigma^2$. The goal is to minimize the first two terms; $\sigma^2$ is the irreducible noise floor.

- **Lasso shrinks coefficients to zero, performing automatic feature selection.** Instead of manually choosing features, let the L1 penalty figure it out. Choose the penalty strength $\alpha$ by cross-validation.

- **Random forests escape the classical tradeoff through averaging.** Each tree is overfit, but their errors point in different directions. Averaging cancels noise without losing signal.

- **Distribution shift: training data $\neq$ deployment data is the root cause of many failures.** Before trusting a model, ask: training data from when, from where, from whom?

- **Forward references:** [Chapter 8](lec08-sampling.qmd) (bootstrap), [Chapter 12](lec12-regression-inference.qmd) (regression inference), [Chapter 16](lec16-backtesting.qmd) (temporal validation), [Chapter 17](lec17-automl-llms.qmd) (ensembles deep dive).

## Study guide

### Key ideas

- **Train/test split** — holding out part of the data to evaluate model performance on unseen data.

- **Validation set** — data used to choose model complexity (distinct from the final test set).

- **Cross-validation (k-fold)** — rotating which of $k$ folds is held out, averaging test scores for a more stable estimate of out-of-sample performance.

- **Overfitting** — the model memorizes training data (including noise) and performs poorly on new data. Training $R^2$ always improves with more features; when features outnumber effective data points, test $R^2$ can degrade dramatically — the gap between train and test performance is overfitting.

- **Underfitting** — the model is too simple to capture the real pattern in the data.

- **Bias-variance tradeoff** — the tension between underfitting (high bias) and overfitting (high variance). For MSE: expected test error = bias$^2$ + variance + $\sigma^2$ (irreducible noise). The goal is to minimize the first two terms; $\sigma^2$ sets the floor.

- **Lasso (L1 regularization)** — adds a penalty $\alpha \sum |\beta_j|$ that shrinks some coefficients to exactly zero, performing automatic feature selection.

- **Ridge (L2 regularization)** — adds a penalty $\alpha \sum \beta_j^2$ that shrinks coefficients toward zero but does not set them exactly to zero; useful when many features contribute small effects.

- **Regularization** — constraining model complexity to reduce overfitting. Lasso and ridge are the two main forms for linear regression.

- **Leave-one-out CV (LOO-CV)** — the extreme case of $k$-fold CV where $k = n$; each observation gets its own fold. Low bias but high variance and computationally expensive.

- **Irreducible noise ($\sigma^2$)** — inherent randomness in the outcome that no model can eliminate. Even the true model faces this floor on test error.

- **Three-way split (train / validation / test)** — training data for fitting, validation data for choosing model complexity, test data for final evaluation. Using the test set for model selection contaminates the performance estimate.

- **Distribution shift** — when data a model encounters at deployment differs systematically from its training data. Common forms: covariate shift, temporal shift, label shift.

### Computational tools

- `train_test_split(X, y, test_size=0.3)` — splits data into training and test sets

- `cross_val_score(model, X, y, cv=5)` — performs 5-fold cross-validation and returns scores per fold

- `Lasso(alpha=1.0).fit(X, y)` — fits a Lasso regression with regularization strength `alpha`

- `LassoCV(cv=5).fit(X, y)` — searches over `alpha` values by cross-validation, selects the best

### For the quiz

You are responsible for: train/test split, cross-validation (how it works and why it's better than a single split), overfitting concept, bias-variance tradeoff (the classical U-shape), Lasso concept (what it does, not the optimization details), distribution shift, and why random forest test error plateaus rather than showing a U-shape.