Lecture 16: When validation isn’t enough

MSE 125 — Applied Statistics

Wednesday, May 20, 2026

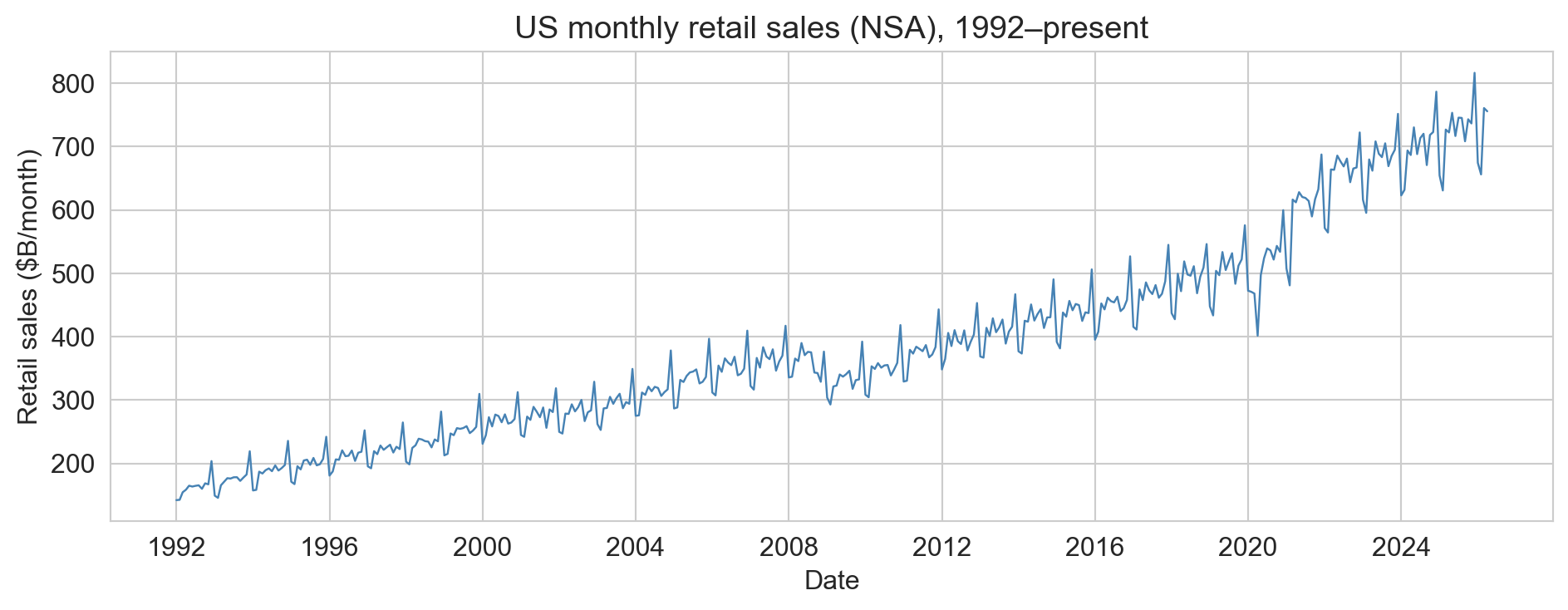

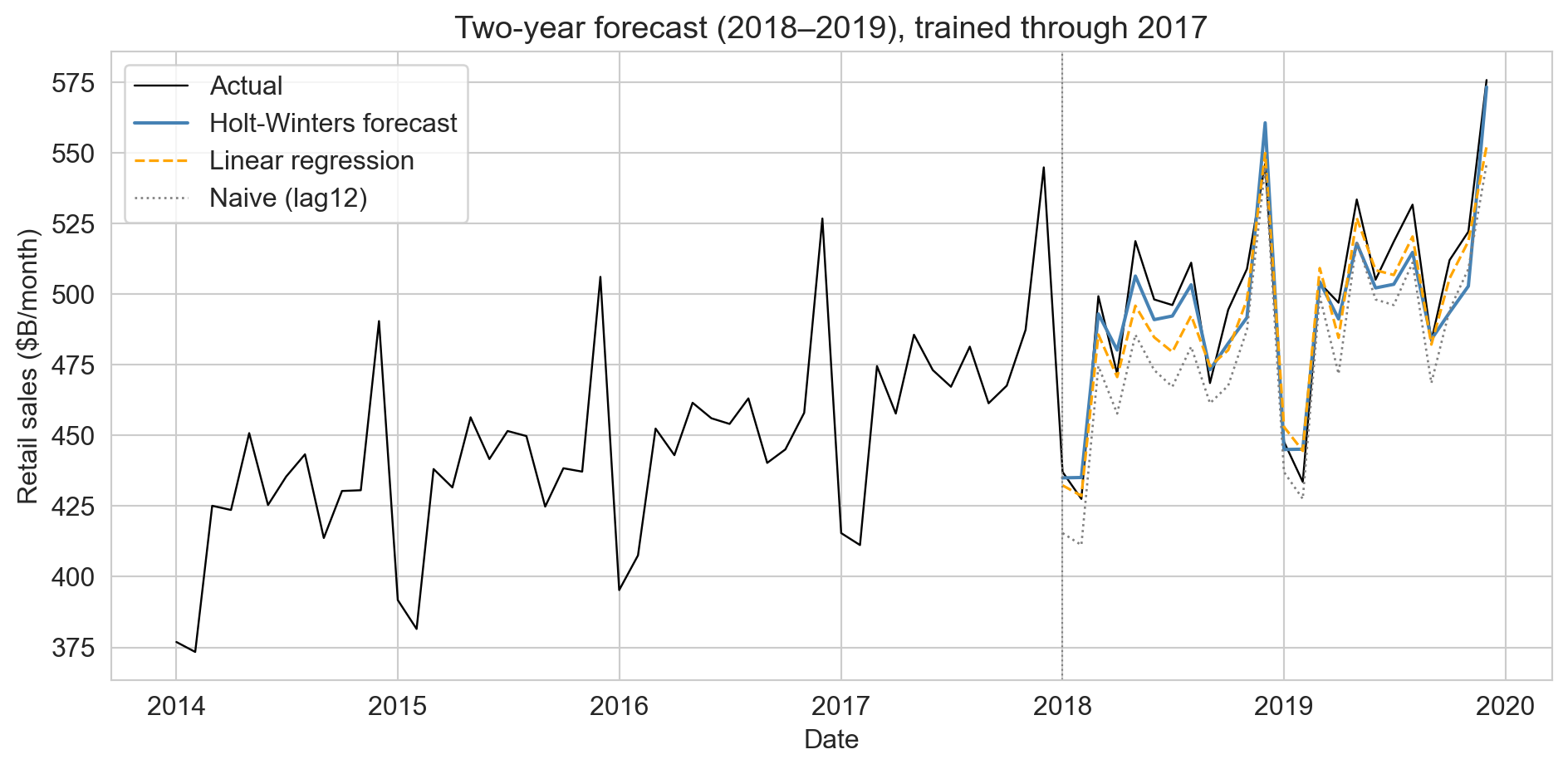

the data: US monthly retail sales

US Census / FRED series RSAFSNA, not seasonally adjusted

- long-run trend: sales grow with population, prices

- annual cycle: sharp December spike, January trough

- short-range autocorrelation: this month ≈ last month

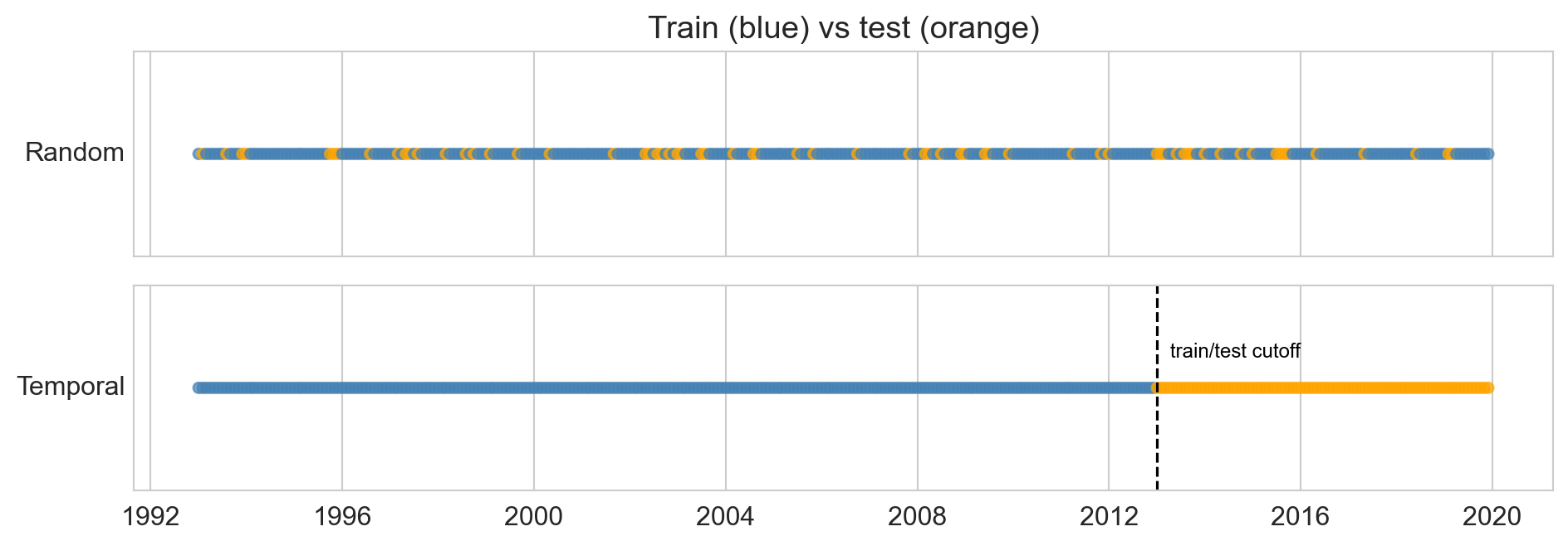

same data, two ways to split

- random: shuffle all months, hold out 20%

- temporal: train early years, test later ones

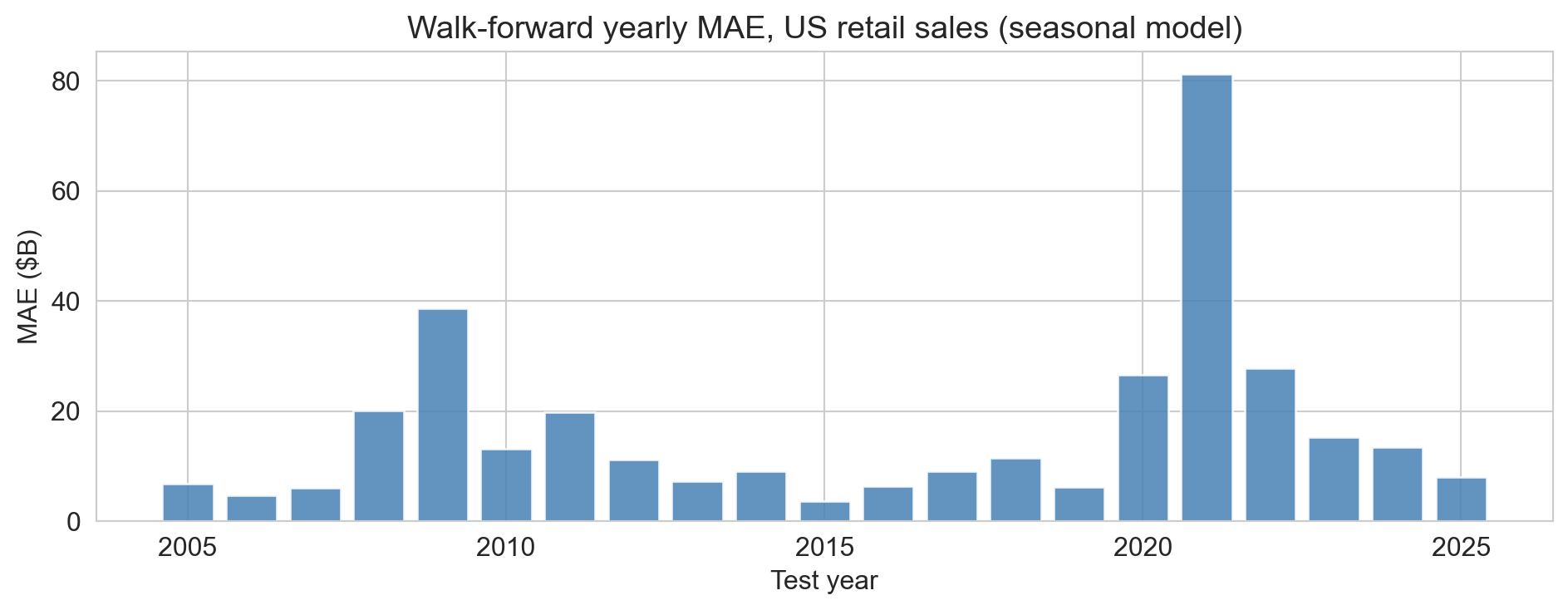

when does the model break?

- low error through the calm years

- spikes: 2008–09 crisis, far larger 2020 pandemic

- a single average MAE would bury these regime changes

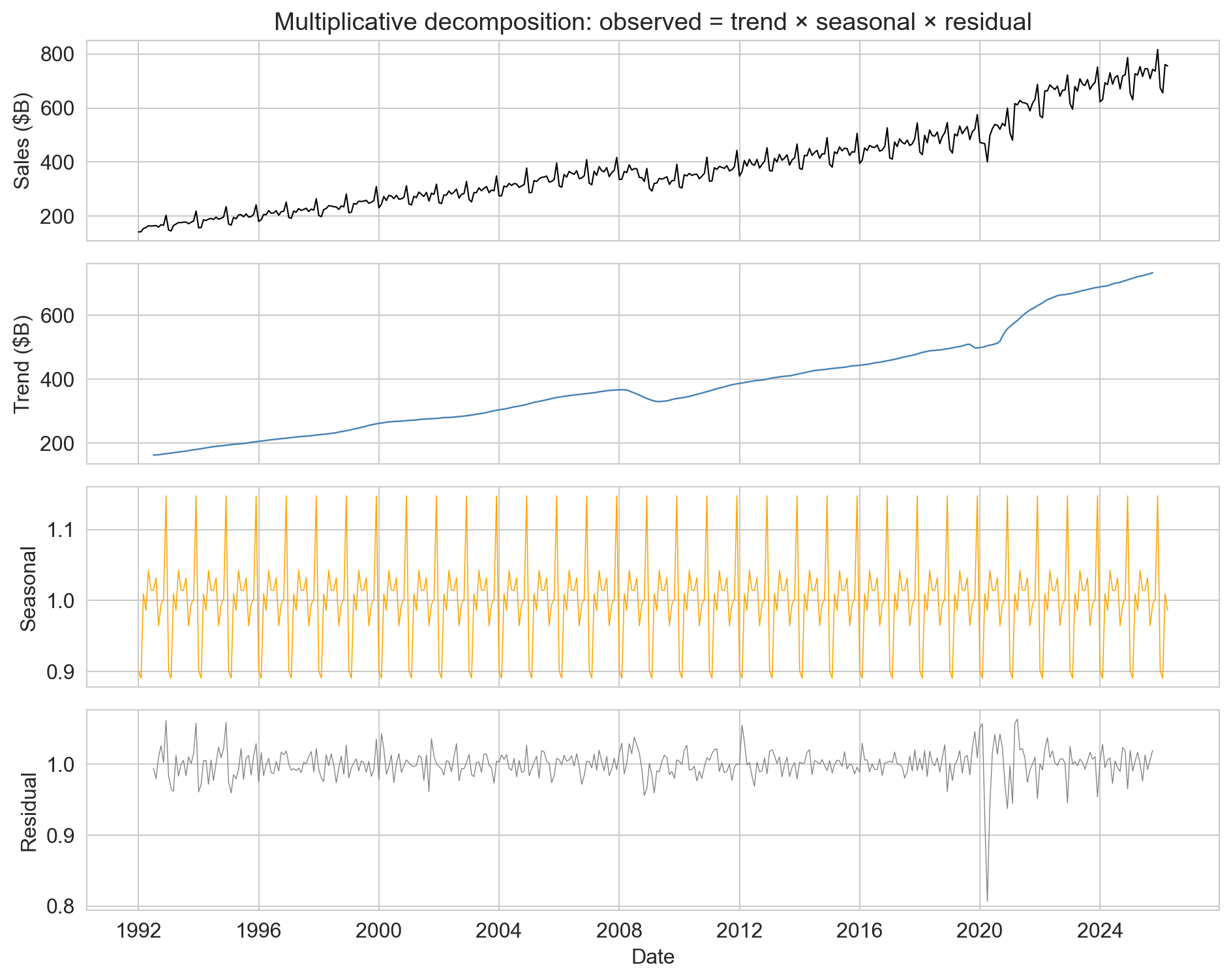

decompose: trend × seasonal × residual

- multiplicative: December is the same percentage above trend each year

- seasonal multiplier: Dec 1.147 (+15% above trend), Feb 0.891

- residual small except the COVID crater

the forecast, and the verdict

Model R² MAE

Naive (lag12) 0.672 $18.2B

Linear regression (lag12+trend) 0.894 $9.5B

Holt-Winters 0.907 $9.0BHolt-Winters wins by tracking the December multiplier. but a better model still doesn’t fix validation: COVID breaks any fit trained through 2019

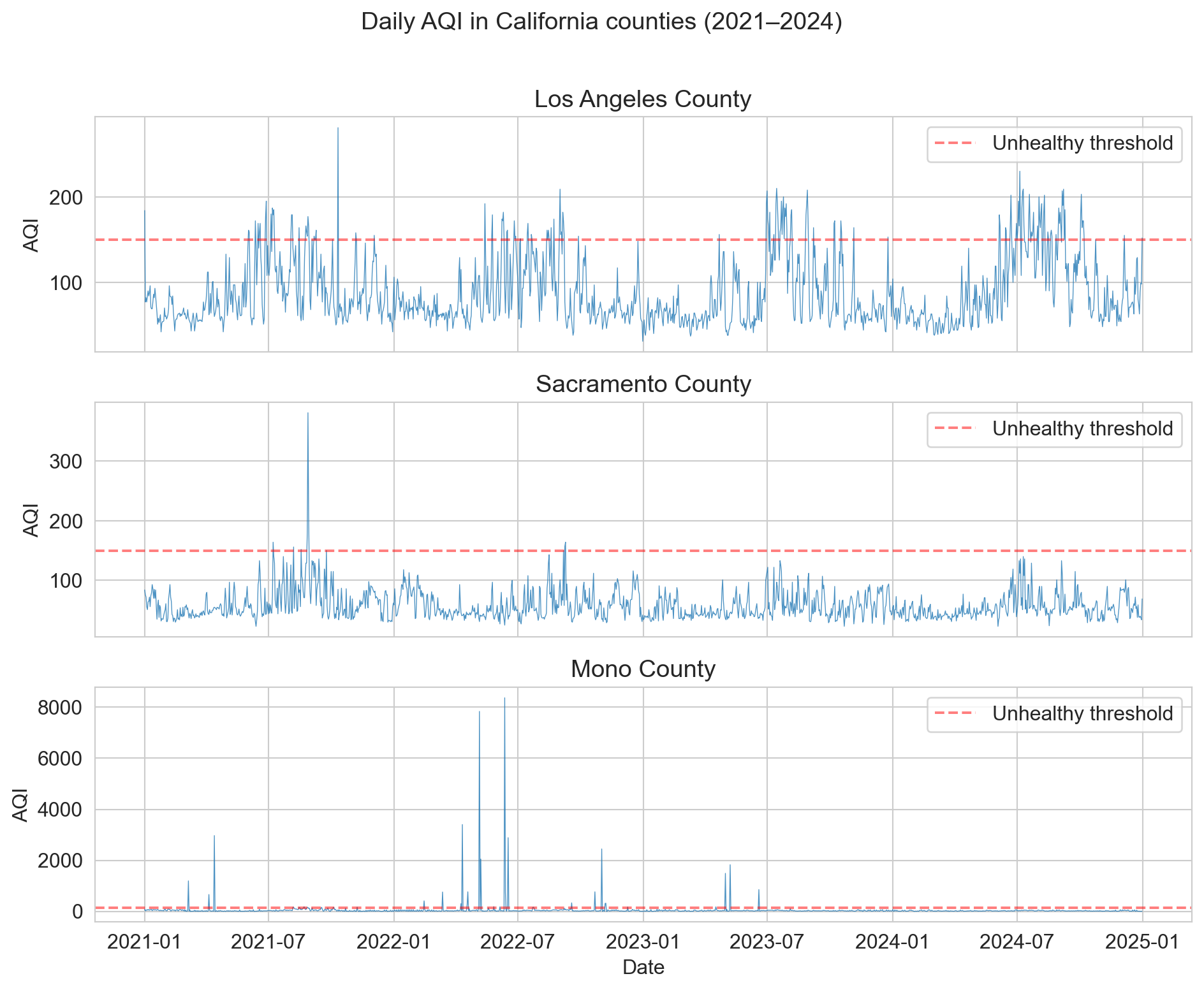

the data: California daily AQI

retail had clean repeating structure. now a series with almost none

- LA, Sacramento: seasonal wildfire spikes on baseline pollution

- Mono County: dust storms push AQI above 8,000

- AQI: 0 clean → 150 unhealthy → 500 hazardous

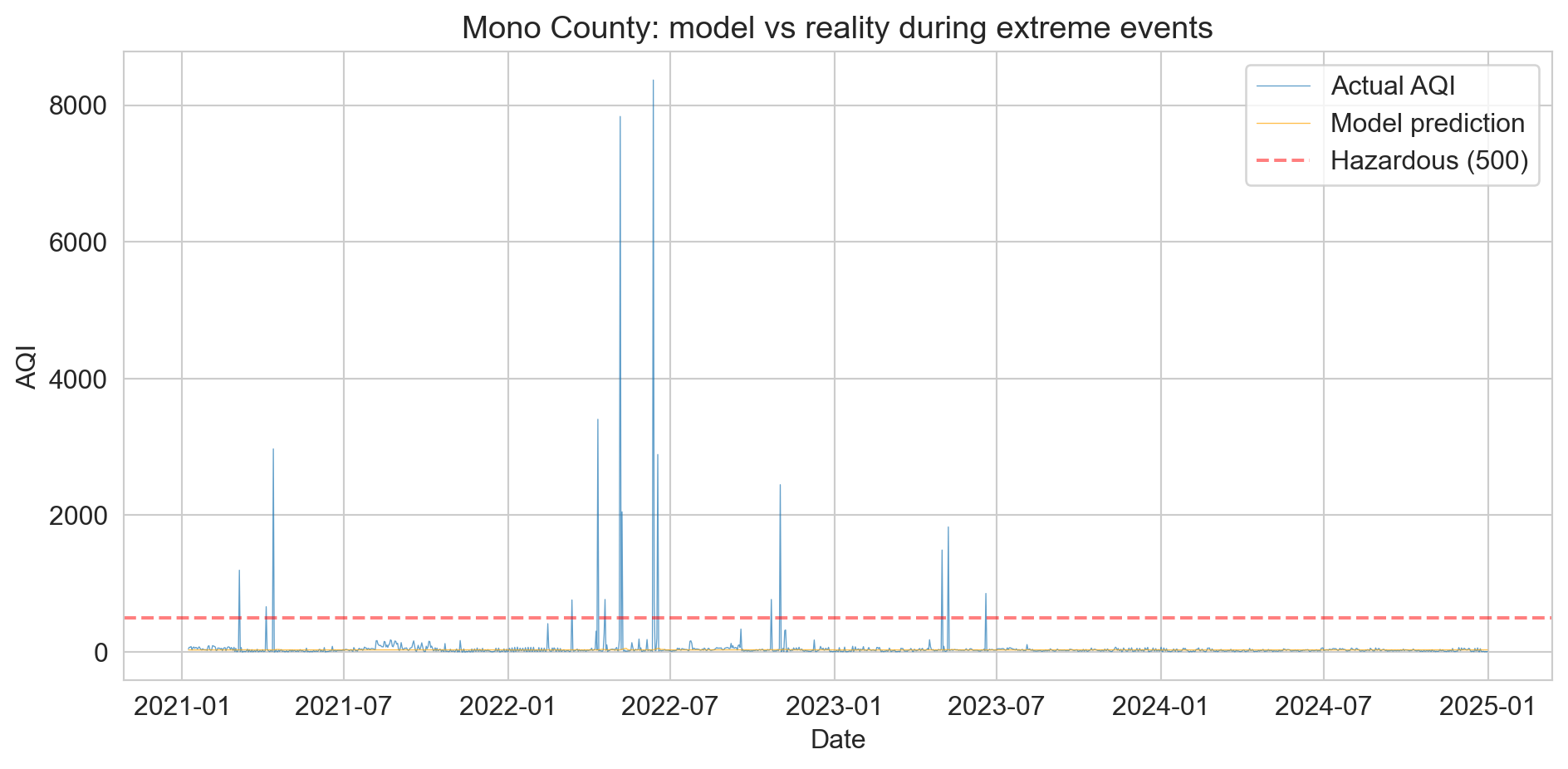

the model flatlines

selected extreme days

Actual AQI Predicted Error

7835 30 7805

3404 30 3374

1196 29 1167coefficient on yesterday’s AQI ≈ −0.0004

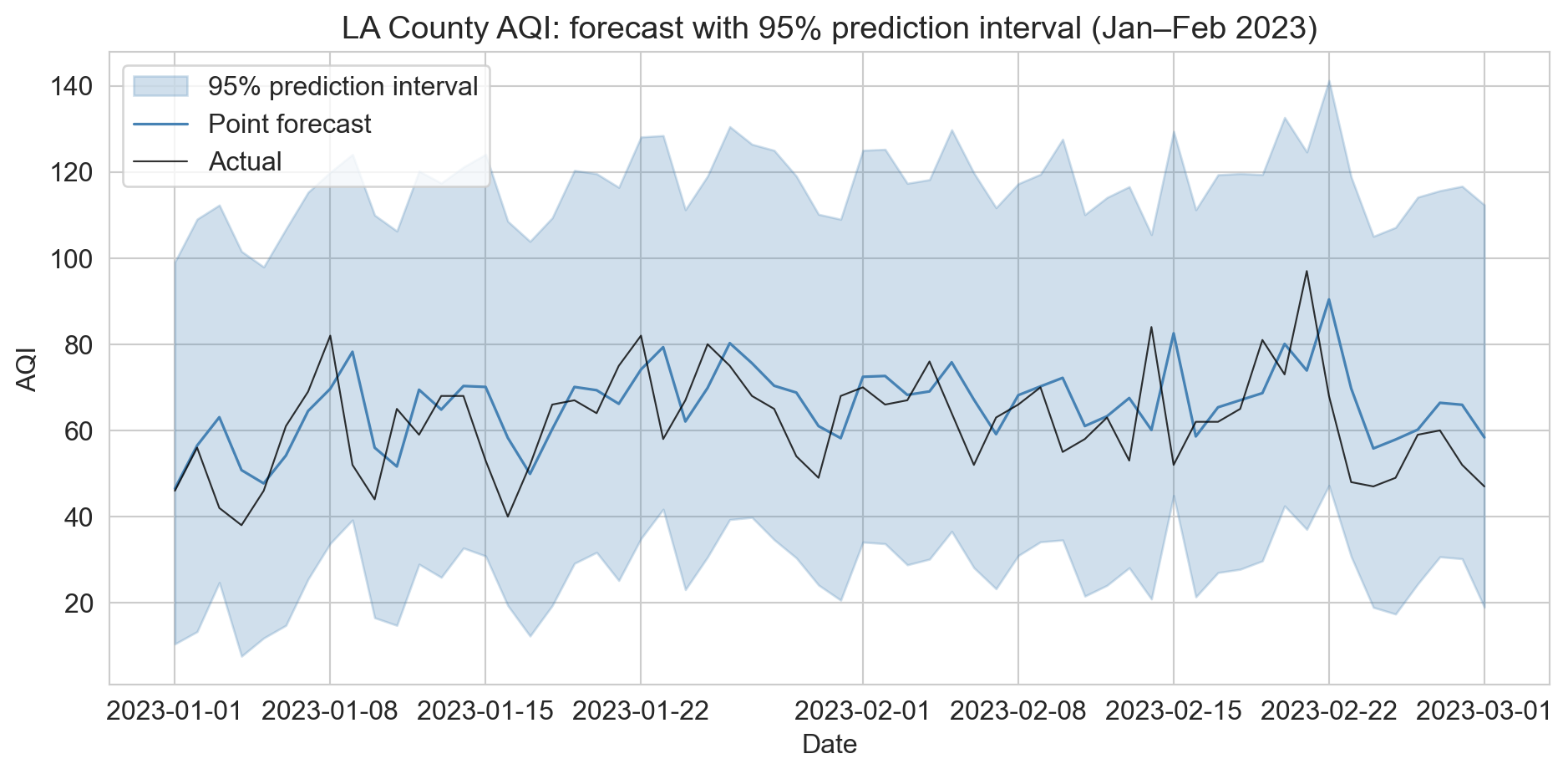

report a range, not a point

- bootstrap from Chapter 8: resample training residuals, add to each forecast

- works for any model: 95% interval here, coverage 93.7%, width 89.5 AQI

- widens for ordinary noise, but blind to regimes never seen (Mono blew past it)

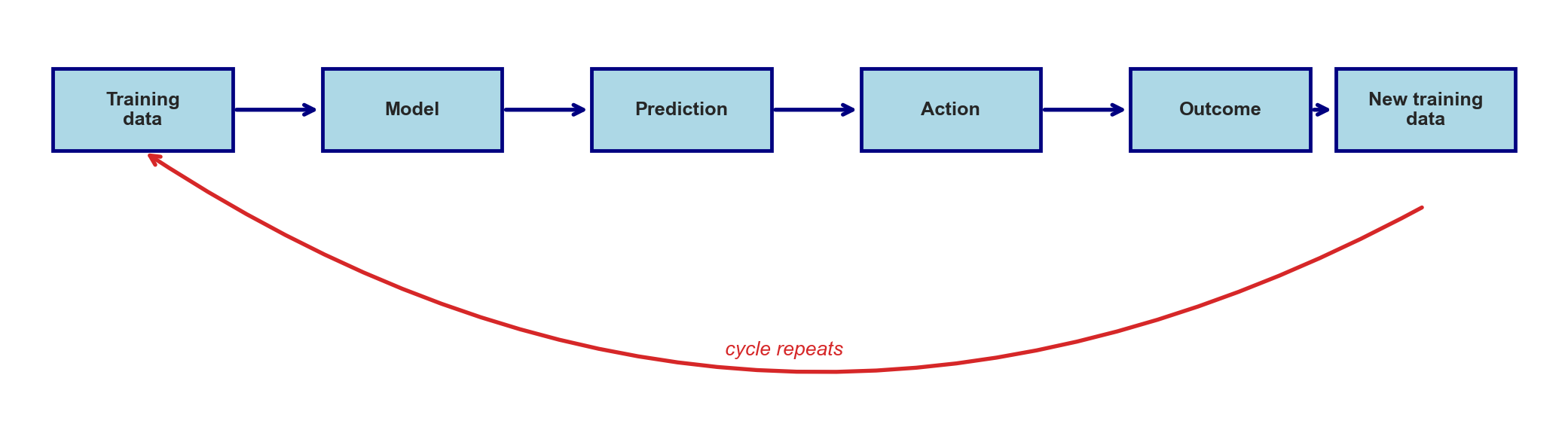

predictive policing

Photo: Mr. Satterly / Wikimedia Commons, CC0

- model flags neighborhood as high-crime

- police patrol it harder

- more patrols → more arrests

- model retrains, “confirms” itself

. . .

the model creates the data that justifies it

a causal arrow runs backward

prediction → action → outcome → new training data → repeat

Weapons of Math Destruction

Photo: GRuban / Wikimedia Commons, CC BY-SA 4.0

three traits together make a WMD:

- outcome not easily measurable

- negative consequences for individuals

- self-fulfilling feedback loop

Cathy O’Neil, Weapons of Math Destruction (2016)

emissions testing

- VW software detected the EPA lab cycle

- full emissions controls only during the test

- on the road: NOx up to ~40× the legal limit

. . .

optimized the test exactly. real-world emissions moved the opposite way

Photo: Mario R. Duran Ortiz / Wikimedia Commons, CC BY-SA 3.0; EPA Notice of Violation 2015

school accountability tests

when evaluations hinge on scores:

- Chicago: answer-altering in ≥ 4–5% of classrooms

- Florida: weak students reclassified as test-exempt

. . .

the score rises without learning rising

Photo: dcJohn / Wikimedia Commons, CC BY 2.0; Jacob & Levitt 2003, Figlio & Getzler 2002

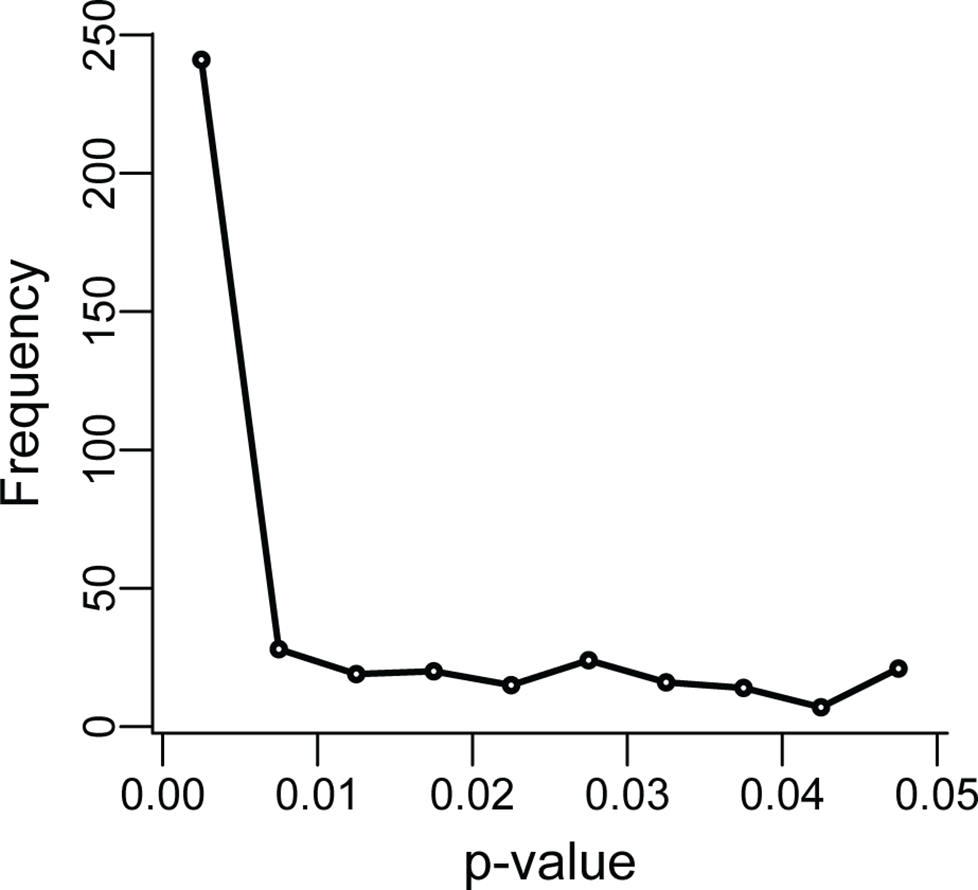

p-hacking

Head et al., PLOS Biology 2015, CC BY 4.0

- p < 0.05 meant to gauge evidence

- careers depend on clearing it

- researchers exploit “degrees of freedom”

. . .

a tell-tale excess of p-values just below 0.05

feedback

what worked? what didn’t? what’s still confusing?