Lecture 14: PCA and Dimensionality Reduction

MSE 125 — Applied Statistics

Wednesday, May 13, 2026

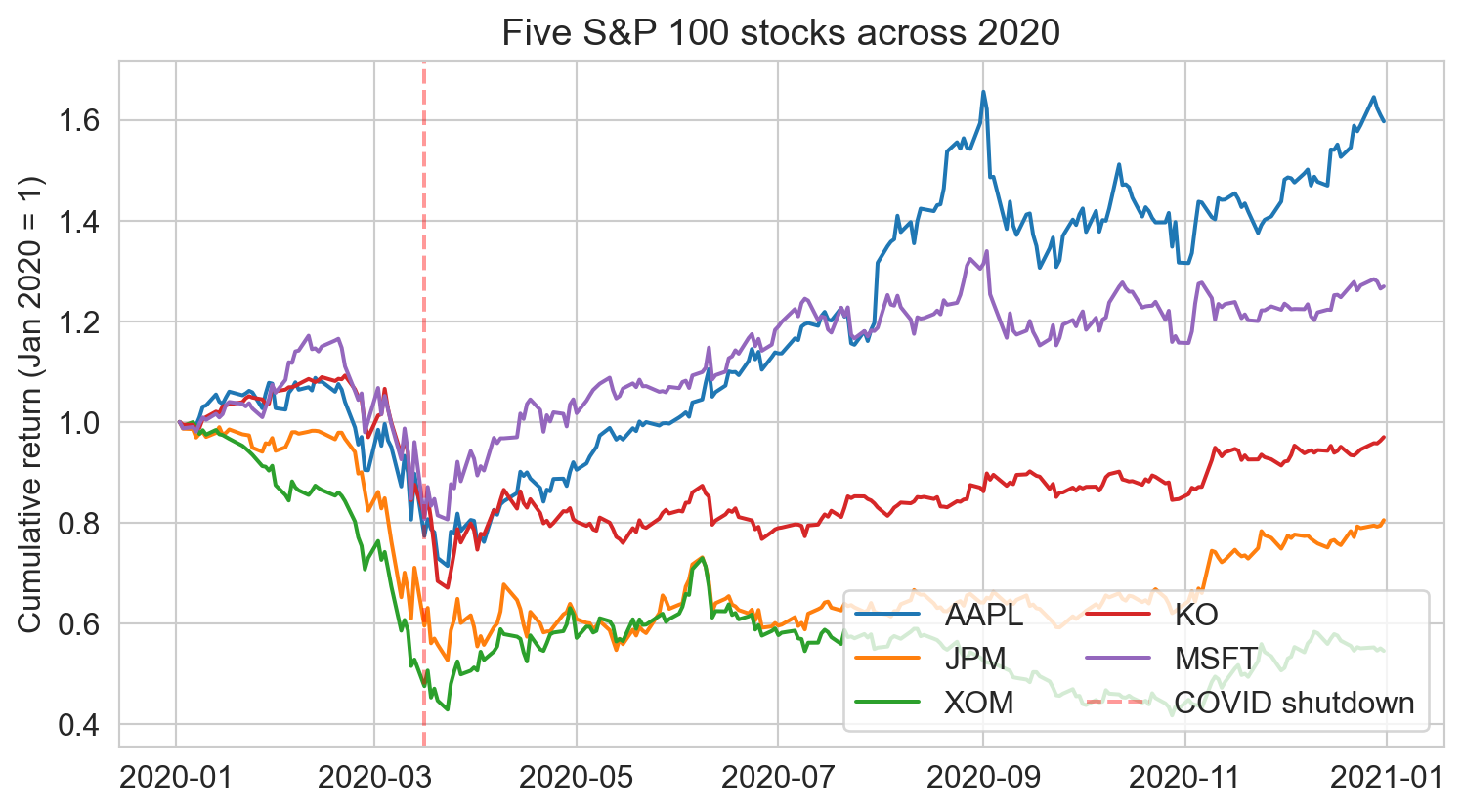

the brief

risk analyst, $5B asset manager

your book: S&P 100 stocks.

last March: every name crashed together

CIO asks: what risk are we really exposed to?

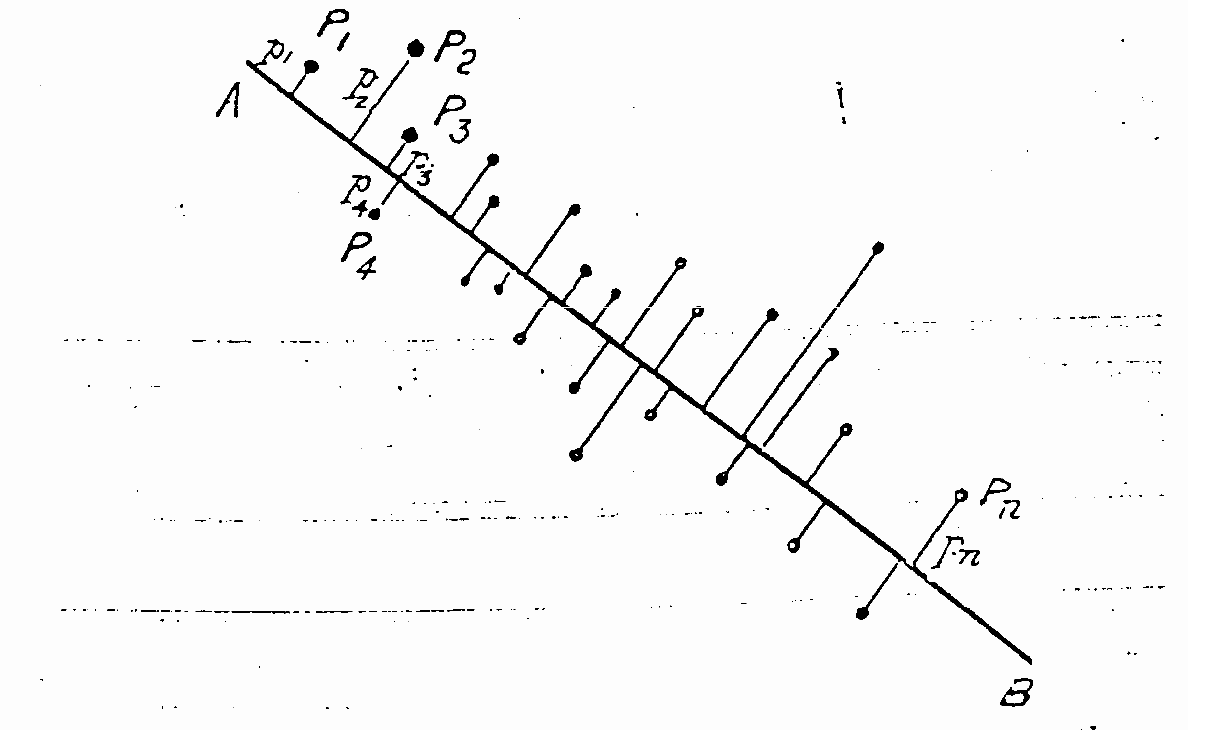

Pearson 1901: same picture, drawn before computers

Pearson, Phil. Mag. 1901

given a cloud of points, what line minimizes the sum of squared perpendicular distances from points to the line?

Pearson answered this in any number of dimensions, with just elementary geometry

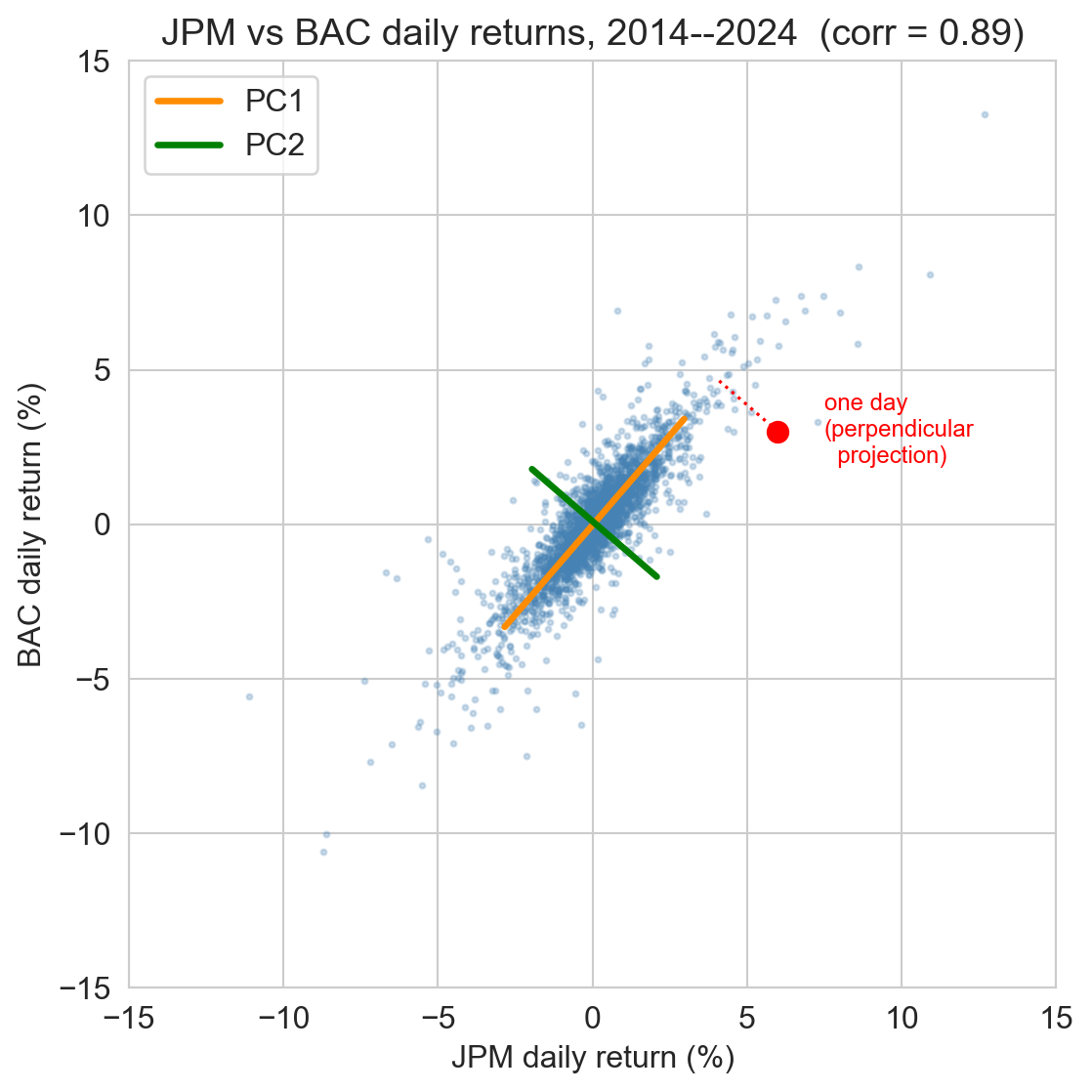

same picture, real data: JPMorgan vs Bank of America

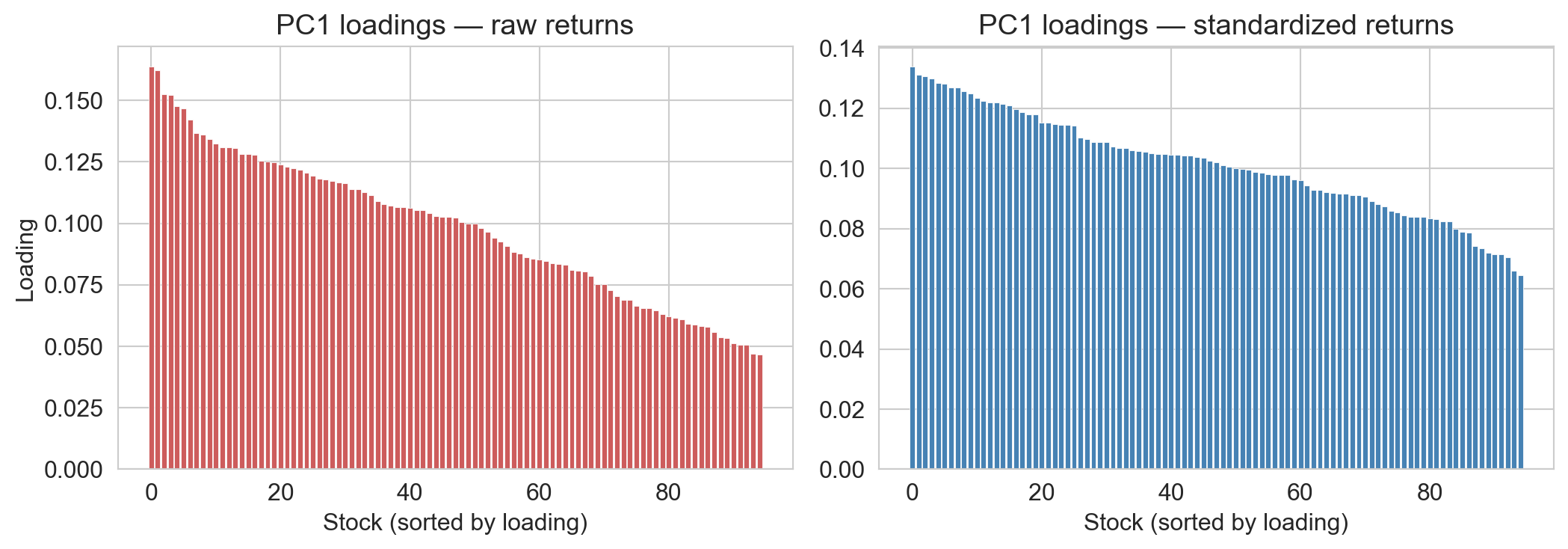

without standardization: high-vol stocks dominate

top 5 by |PC1 loading|

| raw | standardized | ||

|---|---|---|---|

| AMD | 0.164 | BLK | 0.134 |

| NVDA | 0.162 | HON | 0.131 |

| COF | 0.153 | MS | 0.131 |

| TSLA | 0.152 | JPM | 0.130 |

| BA | 0.148 | C | 0.128 |

→ raw: semis, EV, aerospace. the loud names, top 5 hold ~12%

→ standardized: financials. the most market-correlated, top 5 hold ~8.5% (baseline 5.3%)

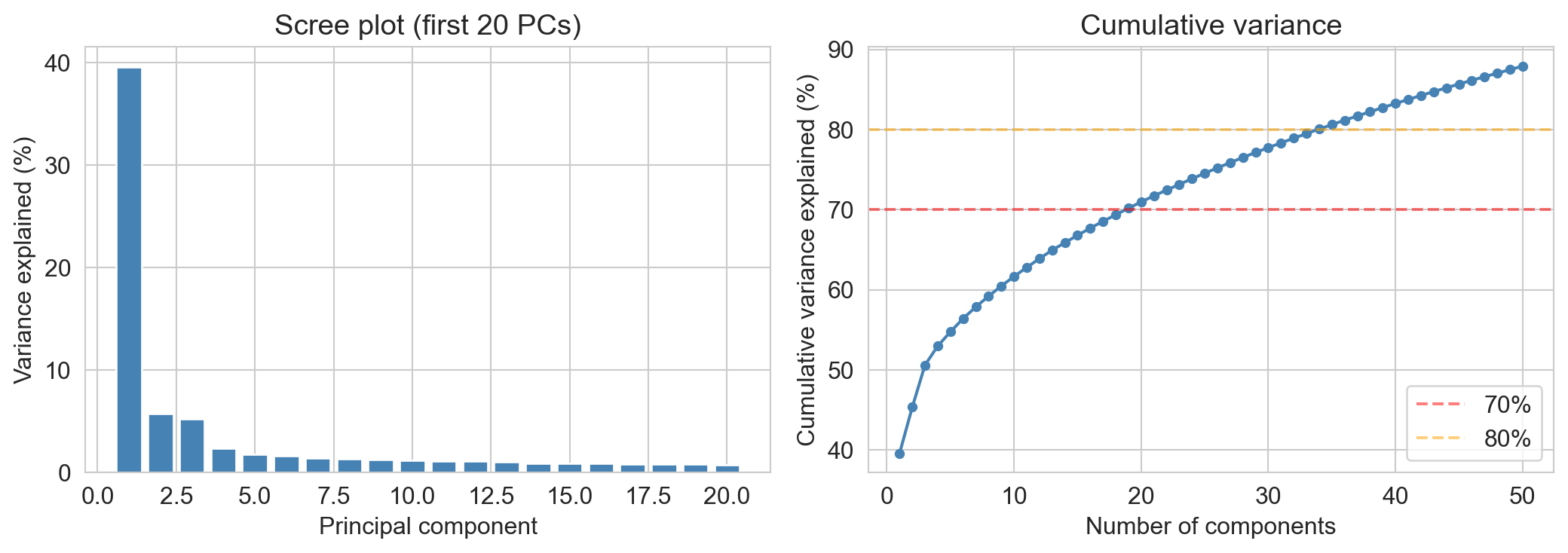

the scree plot: variance per PC

- PC1 alone: ~40% of variance

- 70% needs ~20 PCs; 80% needs ~35

- one big factor + a long flat tail: typical of equity returns

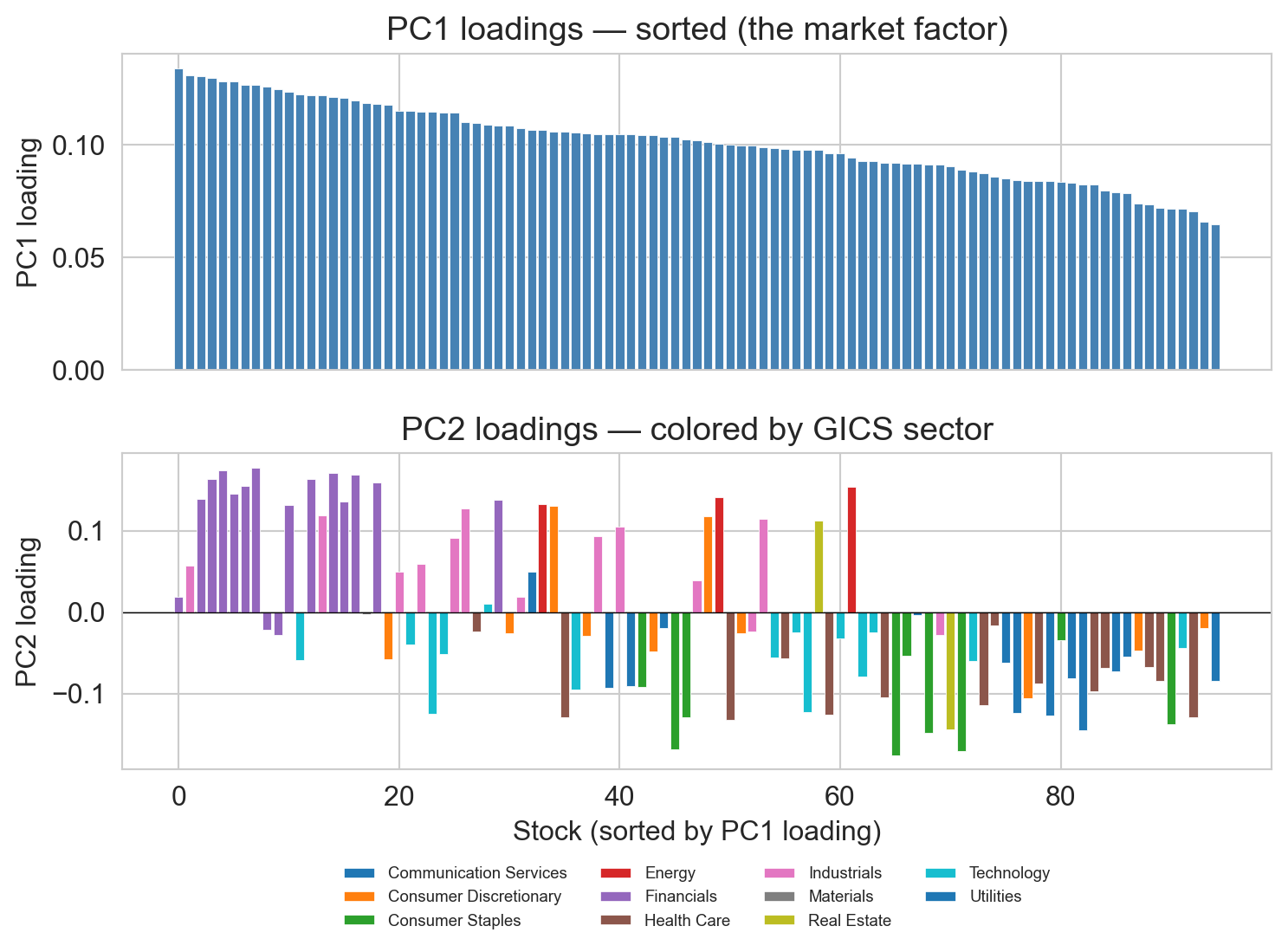

interpret PC1: the market factor

top: every stock loads positively → PC1 is the common up-down move

bottom (PC2, sectors): financials + energy on top; staples + utilities on bottom

→ PC2 = cyclicals vs defensives

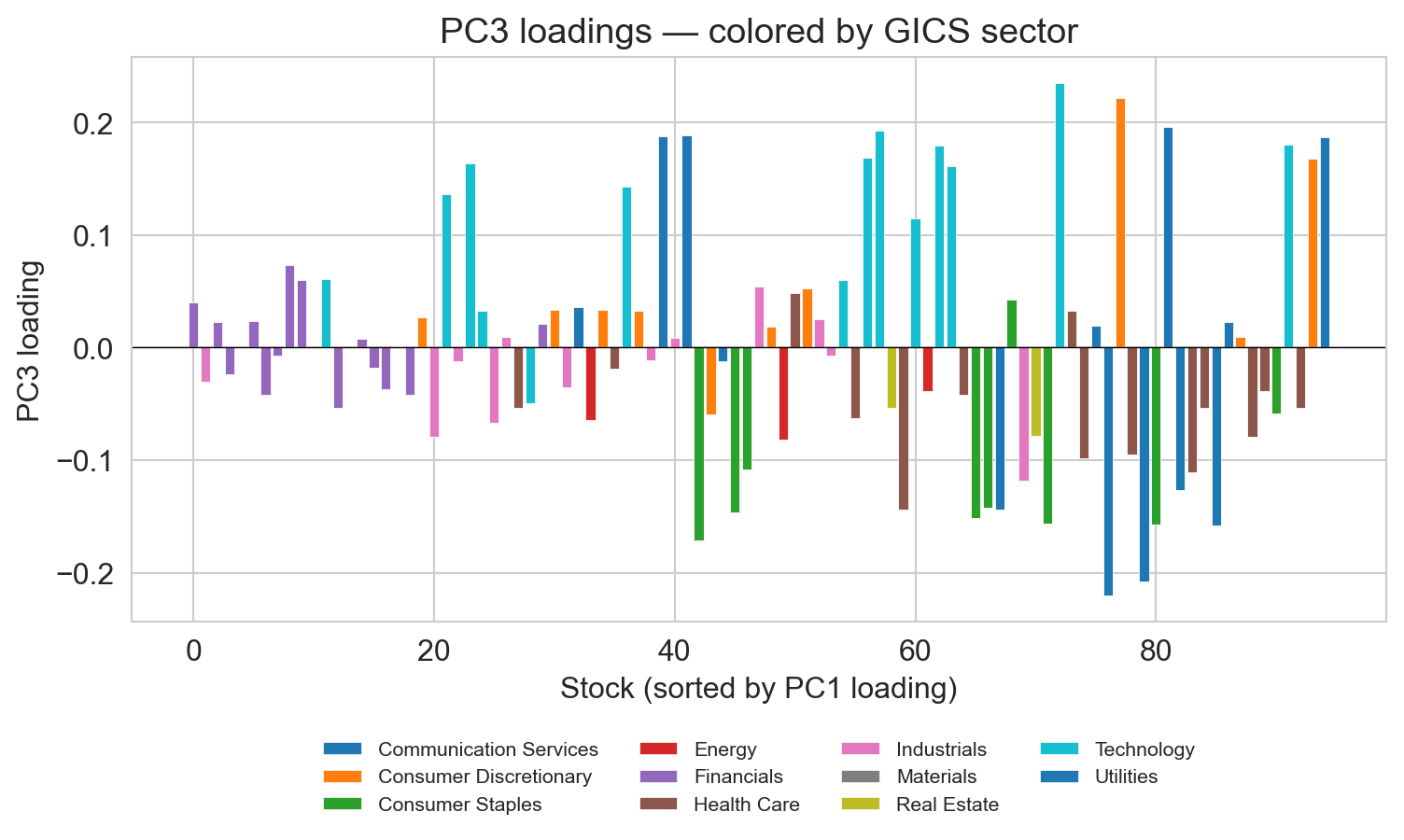

interpret PC3: growth vs yield

positive: NVDA, AMZN, META, GOOGL, ADBE → growth tech

negative: utilities (DUK, SO), staples (KO), high-dividend telecom (VZ) → yield

by PC5 or PC6, the economic story runs out

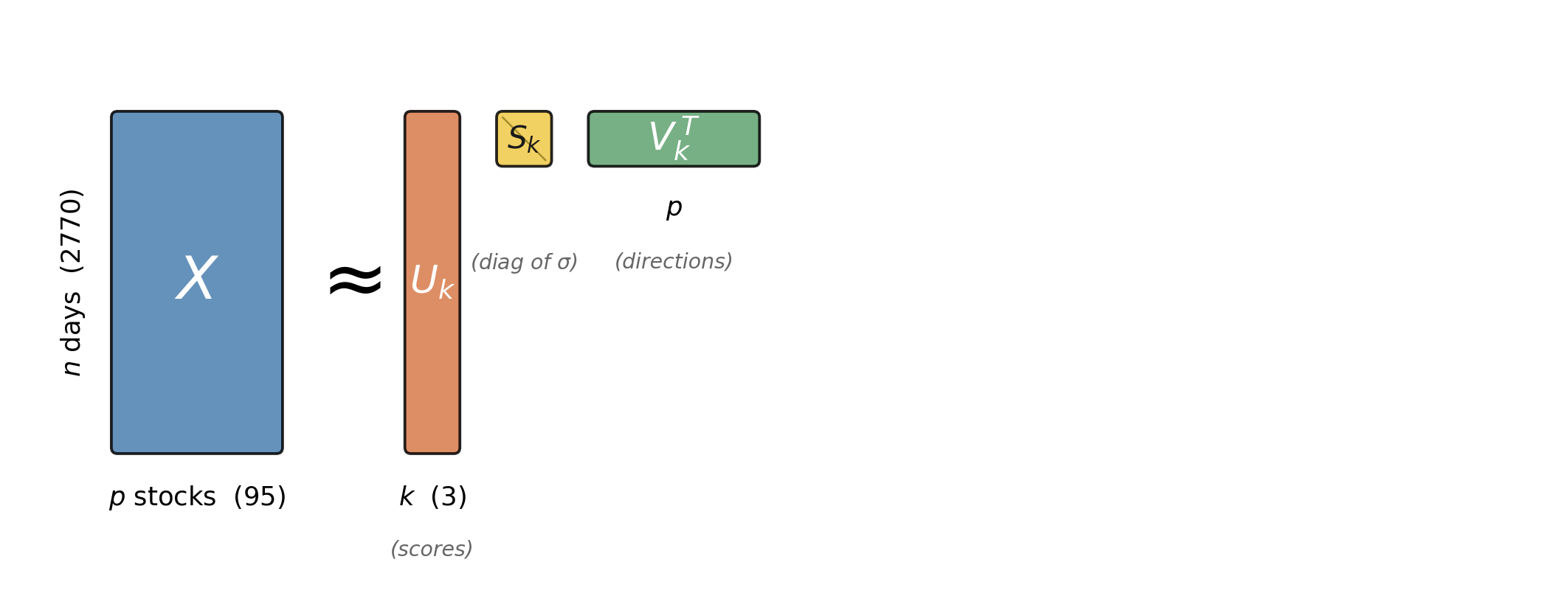

the math: how do we solve it?

data matrix X \in \mathbb{R}^{n \times p}, where row i = x_i

- 2 stocks (earlier): eigendecomposed the 2 \times 2 covariance

- general X: truncated SVD X \approx U_k S_k V_k^T (works directly on X; no covariance to form)

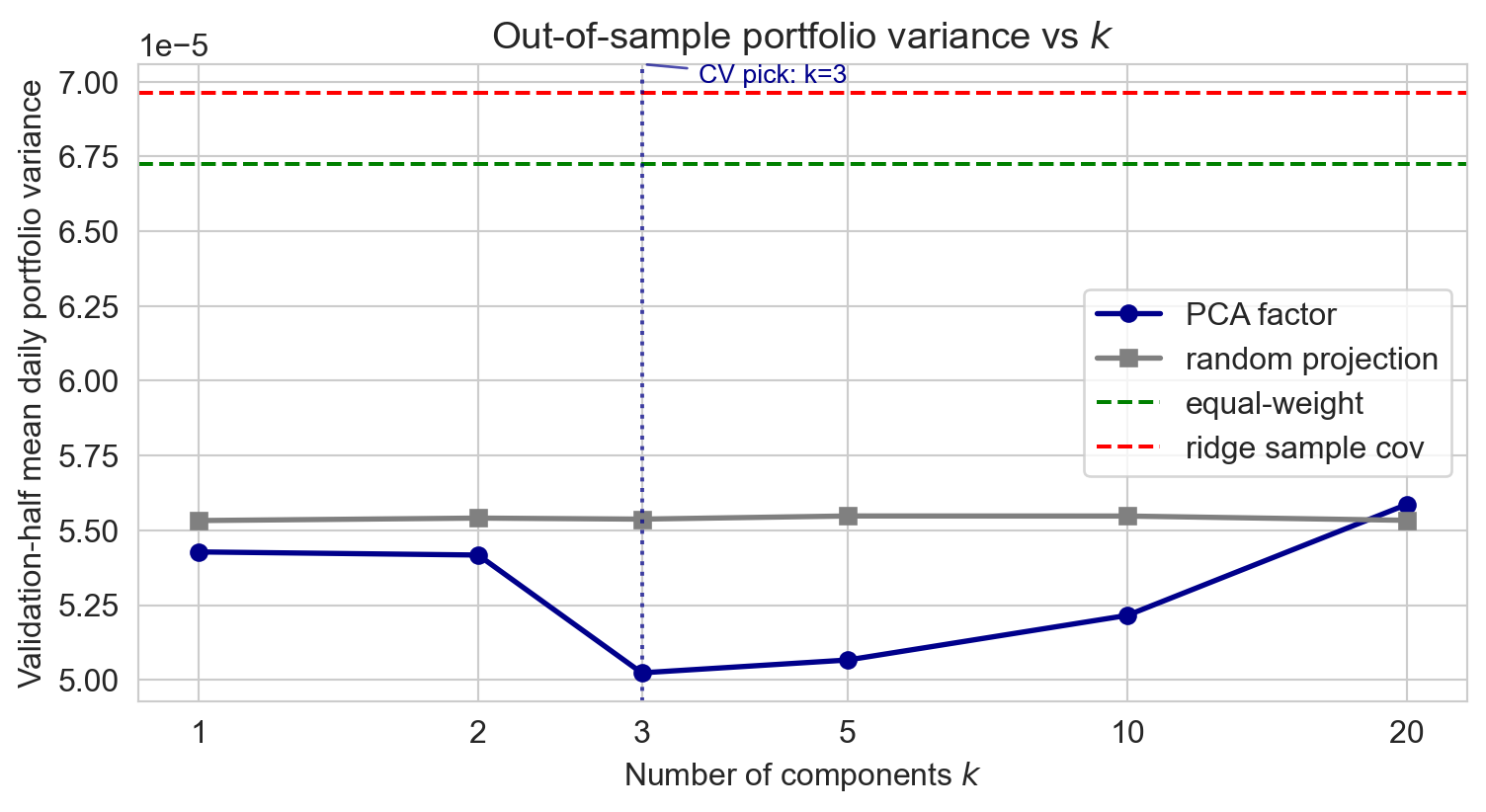

the result: variance vs k

- PCA factor (blue) drops fast 1→3, flat-ish 3→10, rises past 10

- CV picks k = 3: well below scree’s “elbow at 1”

- random projection (gray) lies above PCA throughout: variance-aligned directions matter

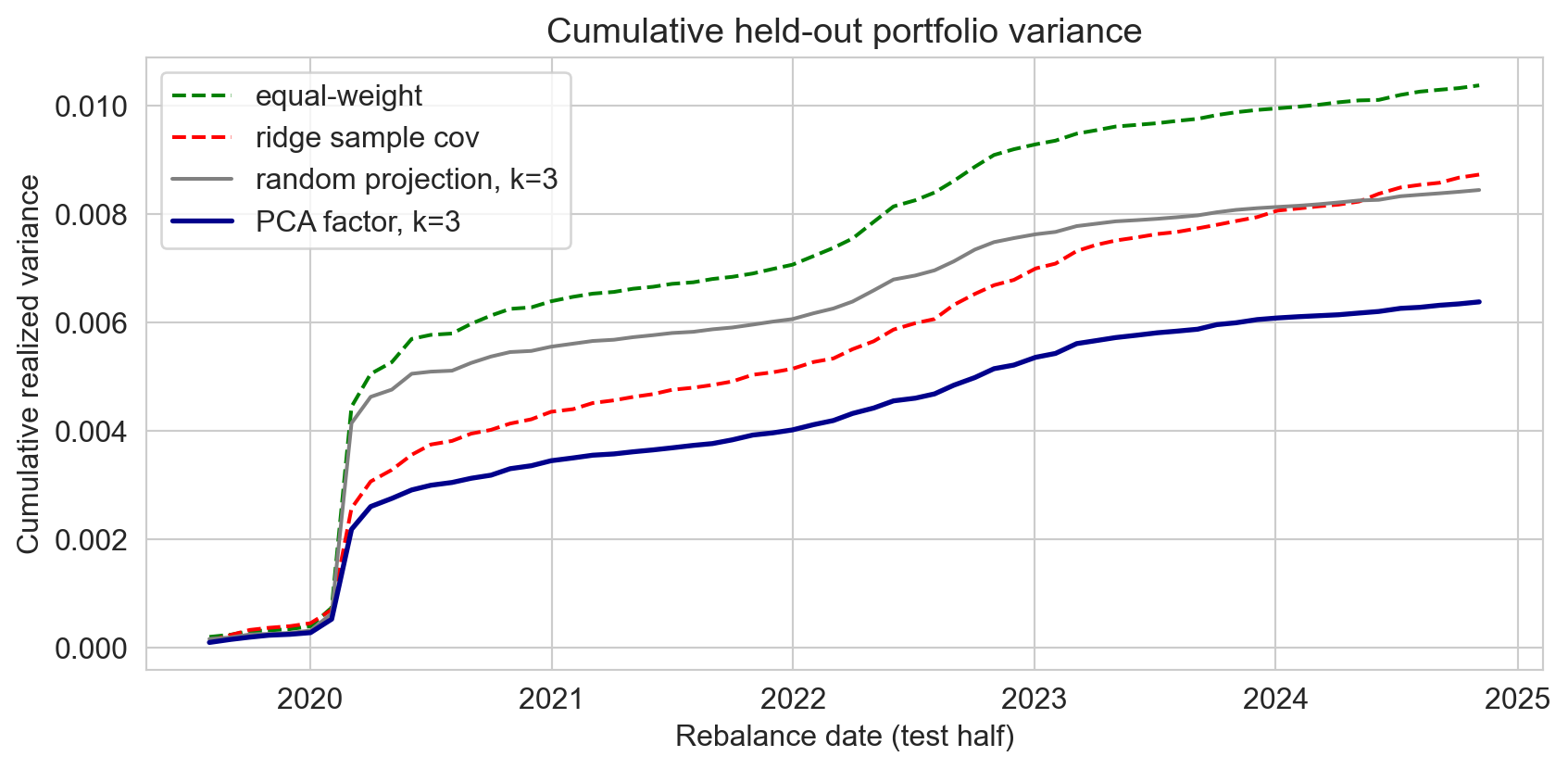

the result: cumulative variance over time

PCA factor portfolio sits lowest the entire test period

every method jumps at COVID; PCA’s jump is smallest

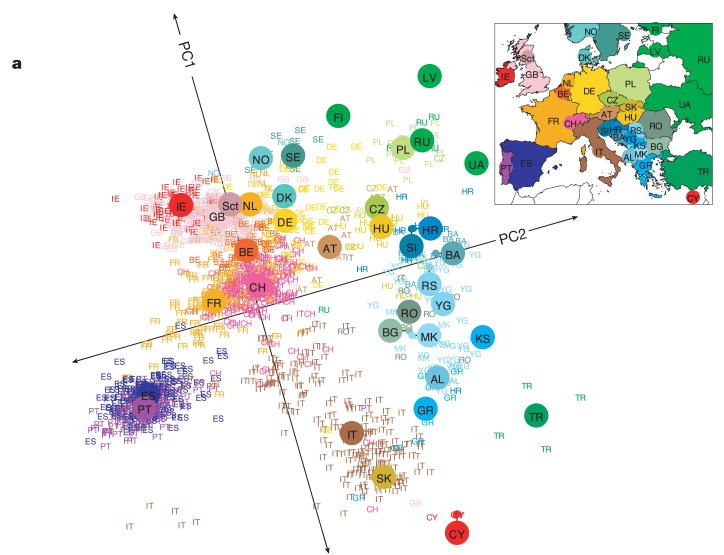

cautionary tale: genes mirror geography

197K SNPs, 1,387 Europeans

no geographic info given to the algorithm

→ it drew a map of Europe (r^2 \approx 0.7)

. . .

→ math result: PCA on spatial data with distance-decaying similarity generically produces these patterns

→ recovering an obvious pattern is not evidence of hidden structure

Novembre 2008; Novembre & Stephens 2008

feedback

what worked? what didn’t? what’s still confusing?