Lecture 4: From the Mean to Simple Regression

Applied Statistics: From Data to Decisions

Professor Madeleine Udell

Wednesday, April 8, 2026

a friend’s Brooklyn listing

text from a friend: “just listed my 2-BR on Airbnb. am I pricing this right?”

first instinct: charge the average

but the average knows nothing about their listing

bigger places should cost more. can we do better?

today

- vectors in data: rows, columns, norms

- predicting with no features: the mean

- predicting with one feature: simple regression

- how good is the fit?: \(R^2\) and correlation

- regression to the mean

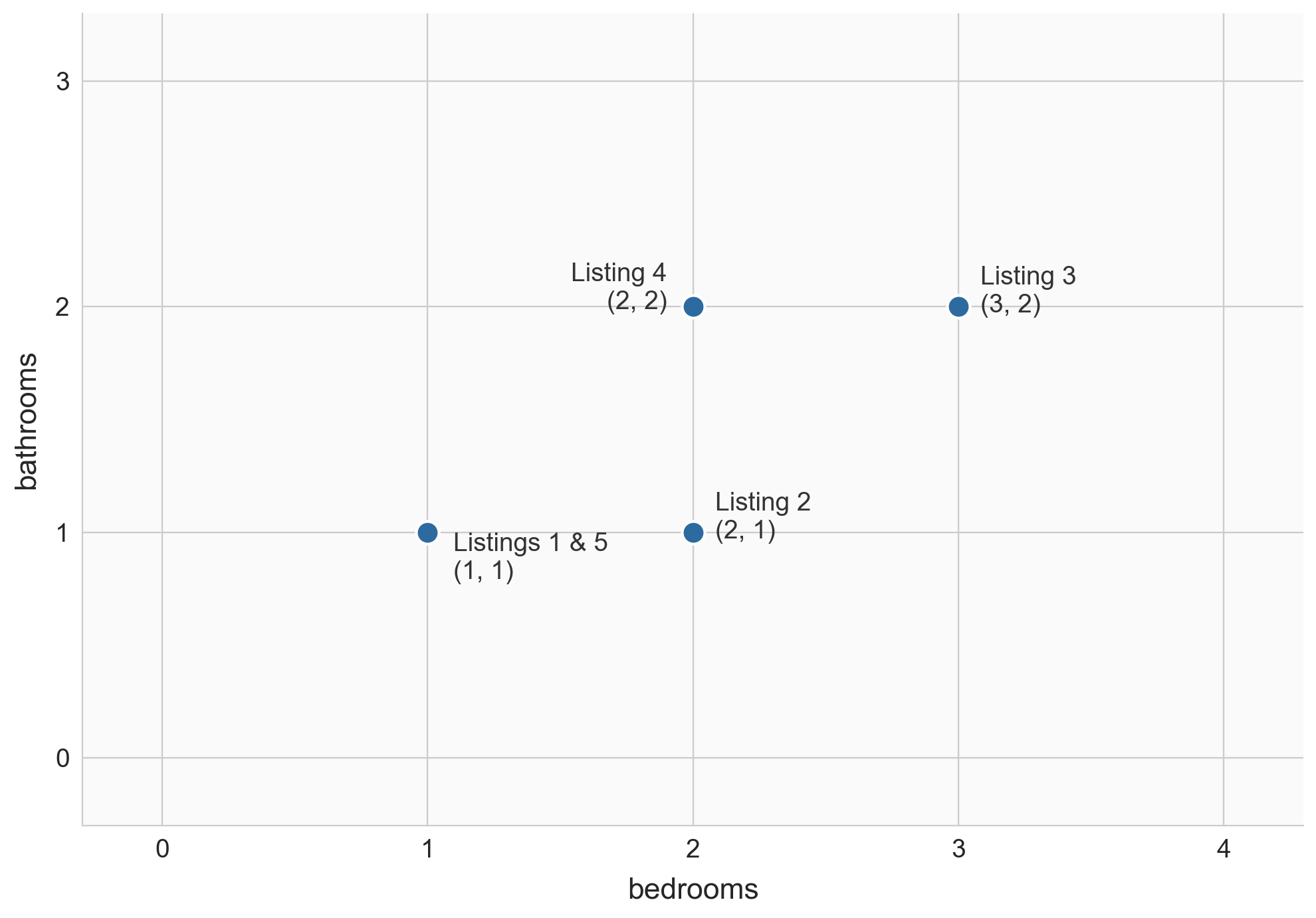

two views of a dataset

| 1 |

1 |

1 |

100 |

| 2 |

2 |

1 |

150 |

| 3 |

3 |

2 |

250 |

| 4 |

2 |

2 |

200 |

| 5 |

1 |

1 |

120 |

- row view: each listing is a point in \(\mathbb{R}^d\), e.g. listing 3 = \((3, 2, 250)\)

- column view: each feature is a vector in \(\mathbb{R}^n\), e.g. bedrooms = \([1, 2, 3, 2, 1]\)

rows as points

![]()

nearby points = similar listings

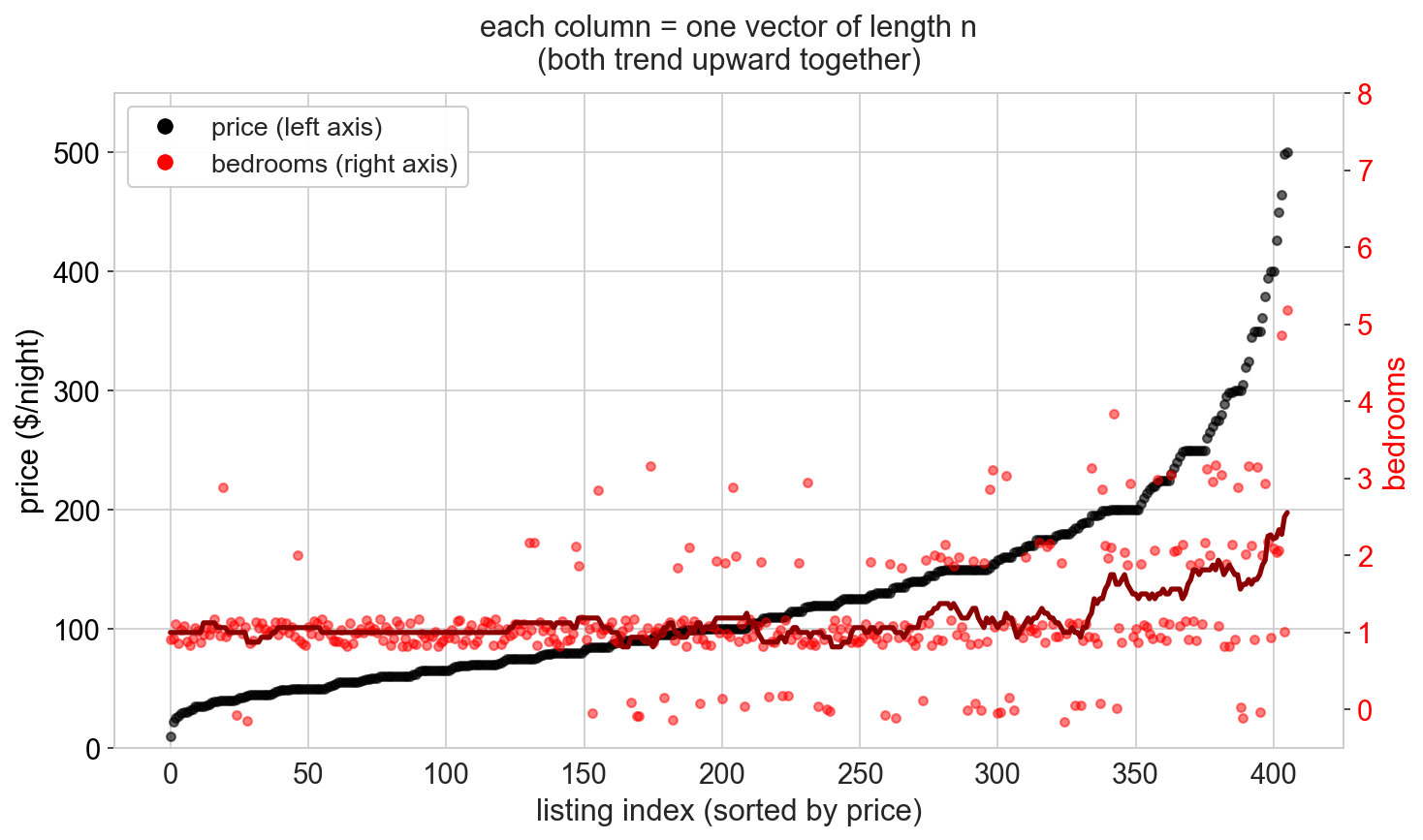

visualizing high-dimensional vectors

a column of \(n\) prices lives in \(\mathbb{R}^n\): too many dimensions to draw as an arrow

index plot: plot value vs listing index

black = price, red = bedrooms (sorted by price): they move together

difference vector

\[\text{listing 3} - \text{listing 1} = (3, 2) - (1, 1) = (2, 1)\]

tells us how they differ: +2 bedrooms, +1 bathroom

but how far apart as a single number?

norm = length of a vector

\(\|v\| = \sqrt{v_1^2 + v_2^2 + \cdots + v_n^2}\)

Pythagorean theorem in \(n\) dimensions.

np.linalg.norm([2, 1])

# sqrt(4 + 1) = 2.24

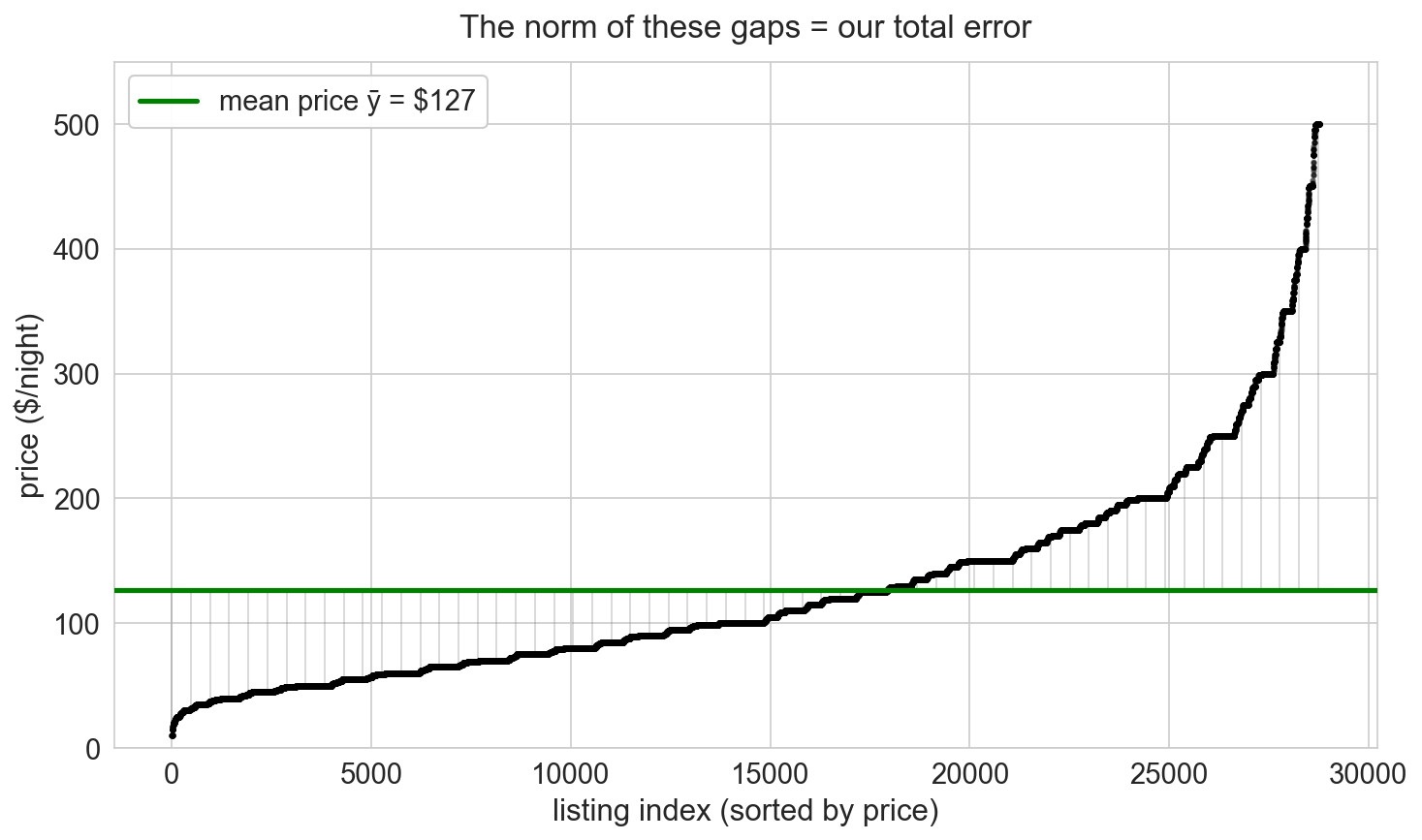

distance = norm of the difference: \(d(u, v) = \|u - v\|\)

the norm will measure prediction error

predict every listing with a single number \(\widehat{y}\)

residual: \(\epsilon_i = y_i - \widehat{y}\), one error per listing

\(\|\epsilon\|\) measures total prediction error

what does it mean for two Airbnb listings to be “similar”?

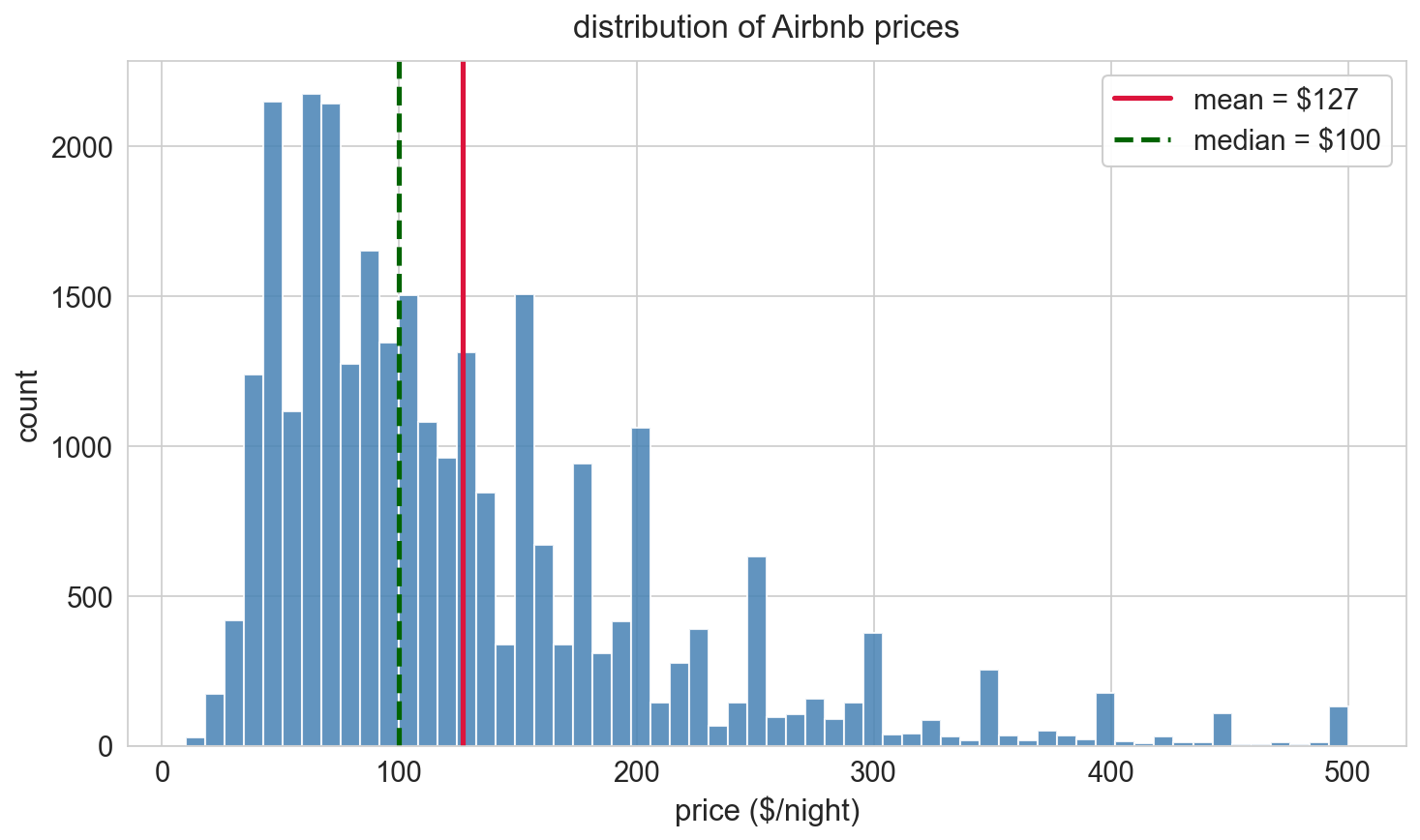

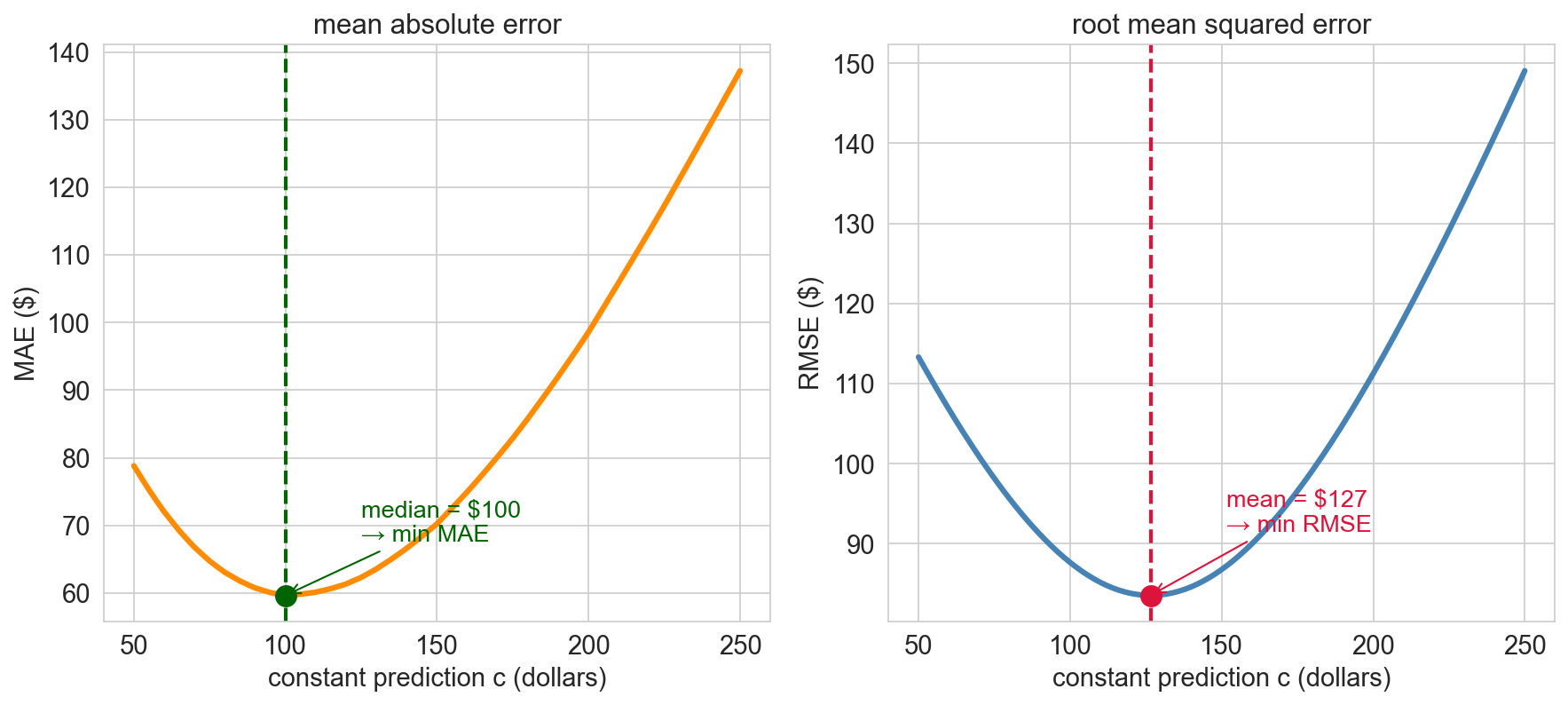

predicting with no features

the simplest predictor: a constant

\(n\) prices. what single number \(\widehat{y}\) should we guess for every listing?

two natural losses

minimize absolute error or squared error?

absolute → median; squared → mean

why should the mean win?

before the proof, a moment of reflection:

as \(c\) moves through the data, what happens to the derivative of \((y_i - c)^2\)?

why does that force a balance exactly at \(\bar{y}\)?

why squared error gives the mean

\[\frac{d}{dc}\sum_i (y_i - c)^2 = -2\sum_i (y_i - c) = 0\]

\[\Longrightarrow \quad c = \frac{1}{n}\sum_i y_i = \bar{y}\]

the mean is the optimal constant predictor under squared error

notation

- \(y = (y_1, \ldots, y_n)\): response vector (actual prices)

- \(\widehat{y}\): prediction vector

- \(\bar{y} = \frac{1}{n}\sum_i y_i\): sample mean

- \(\epsilon = y - \widehat{y}\): residual vector

- \(\beta_0\): intercept

for the constant model: \(\widehat{y}_i = \beta_0\), and the best \(\widehat{\beta}_0 = \bar{y}\)

residuals sum to zero

when \(\widehat{y}_i = \bar{y}\):

\[\sum_i \epsilon_i = \sum_i (y_i - \bar{y}) = n\bar{y} - n\bar{y} = 0\]

in vector notation:

\[\mathbf{1}^T \epsilon = 0\]

the residual is orthogonal to the ones vector: our first normal equation

squared error → conditional mean

same argument, applied within each slice of \(x\):

squared-error regression estimates \(\mathbb{E}[Y \mid X = x]\)

(absolute error → conditional median; other losses → other summaries)

when should you predict with the mean vs the median?

- real estate prices: mean or median?

- insurance claims: mean or median?

- what’s the difference between “typical” and “average”?

predicting with one feature

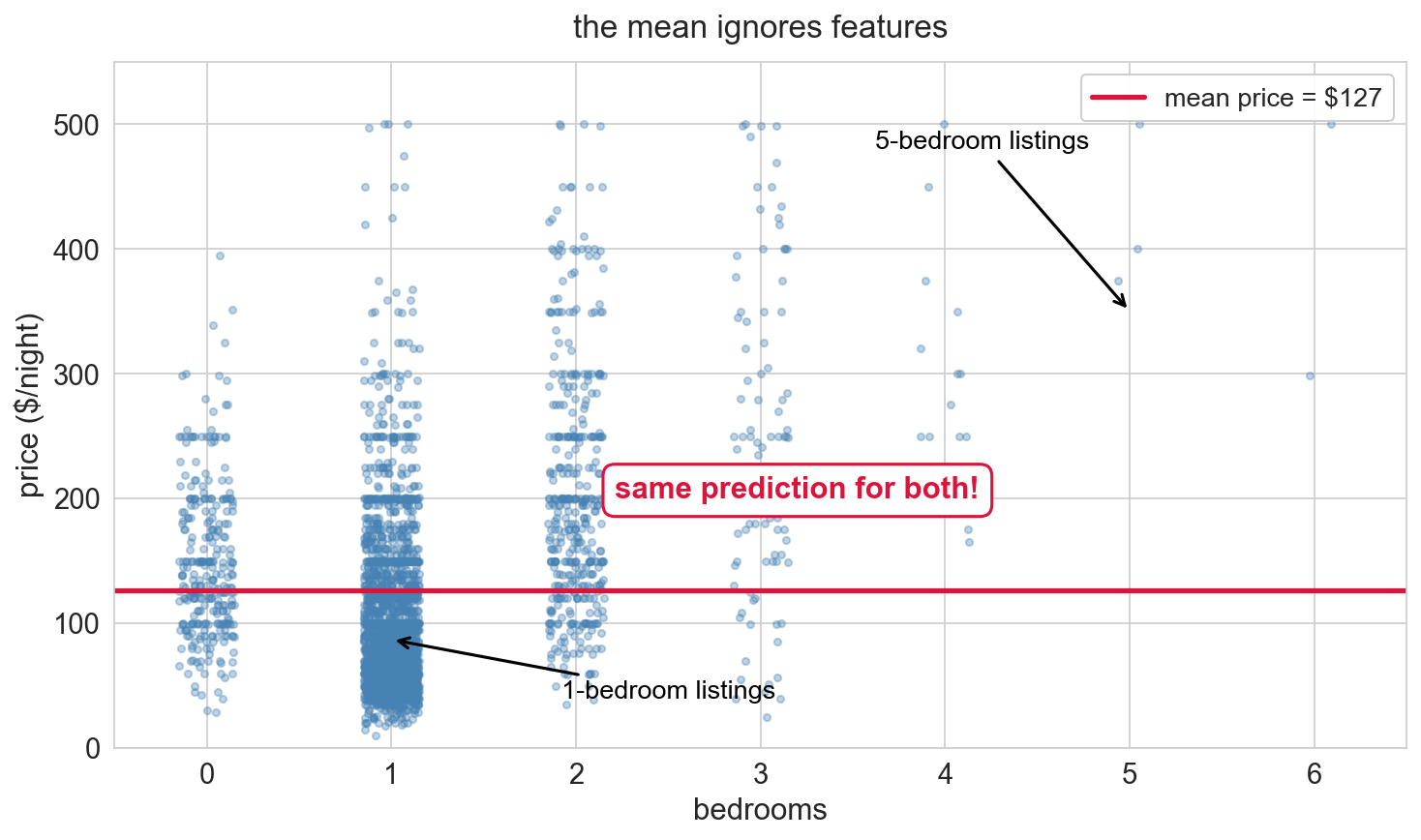

the mean ignores bedrooms

![]()

a 5-bedroom apartment and a studio get the same prediction

a linear combination of two columns

\[\widehat{y}_i = \beta_0 + \beta_1 \, x_i\]

\(\widehat{y}\) is a linear combination of \(\mathbf{1}\) and \(x\):

\[\widehat{y} = \beta_0 \, \mathbf{1} + \beta_1 \, x\]

the span: all reachable predictions

\(\text{span}(\mathbf{1}, x) = \{\beta_0 \mathbf{1} + \beta_1 x : \beta_0, \beta_1 \in \mathbb{R}\}\)

all lines you could draw through the scatter plot

every \((\beta_0, \beta_1)\) traces a different line. which one is best?

before you see any candidate lines: what would “best” look like?

many lines are possible: which is best?

![]()

- red, blue: too steep at the low end

- purple: slopes the wrong way

- green: closer but still arbitrary

we need a principled criterion. it turns out to be geometric

switch to the column view

\(y\), \(\mathbf{1}\), and \(x\) all live in \(\mathbb{R}^n\): one coordinate per listing

\(\text{span}\{\mathbf{1}, x\}\) = a flat plane floating in \(\mathbb{R}^n\)

every line you could draw = one point on that plane

the actual price vector \(y\) sits off the plane: no line fits every listing perfectly

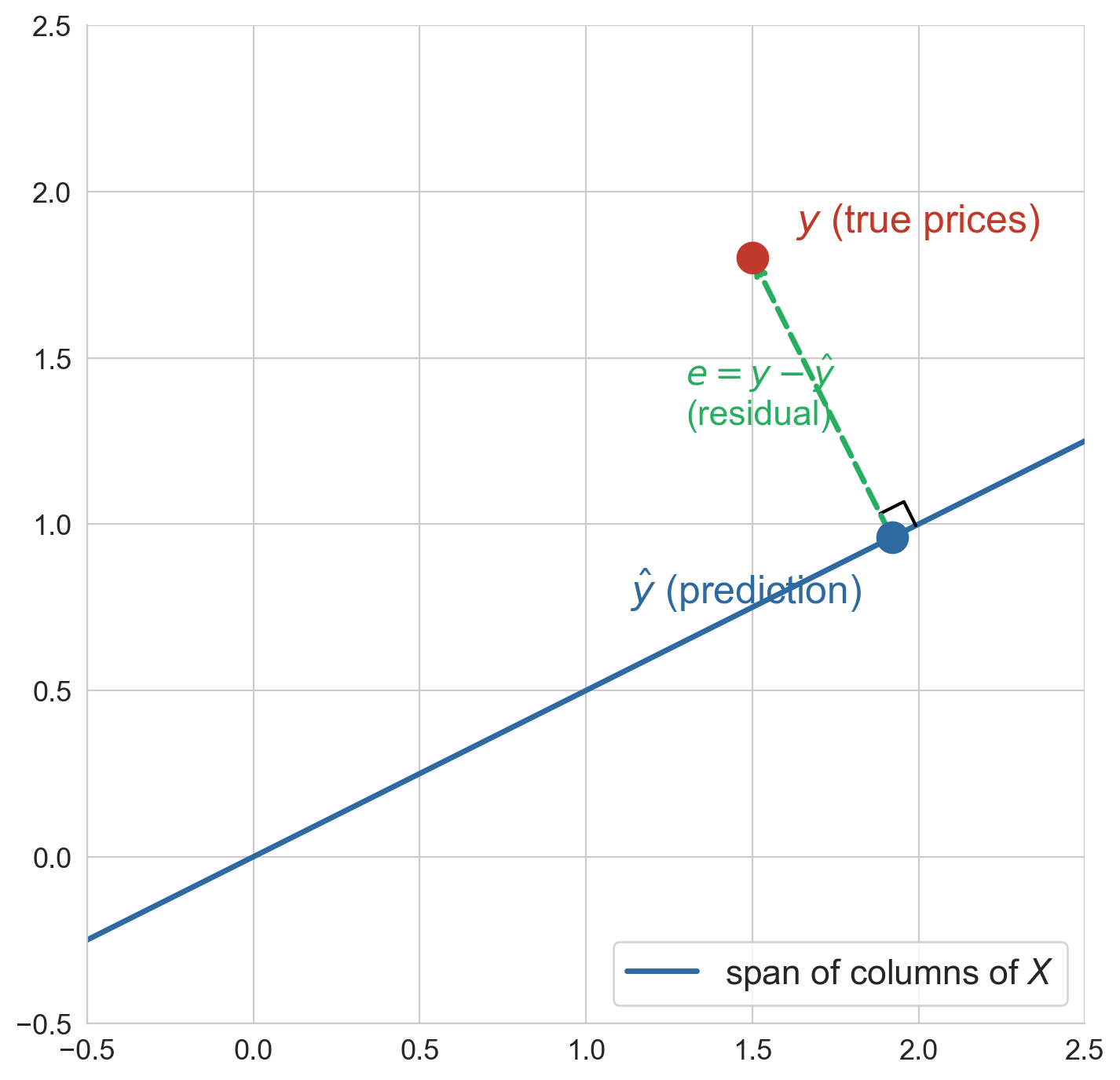

the geometric view: projection

![]()

- \(y\) is a point in \(\mathbb{R}^n\)

- \(\text{span}\{\mathbf{1}, x\}\) is a plane through the origin

- the closest point in the plane is the best prediction

- the residual \(\epsilon\) is perpendicular to the plane

the inner product

Inner product (dot product)

\(u^T v = \sum_{i=1}^n u_i v_i\)

- positive → same direction

- zero → orthogonal

- negative → opposite directions

take \(u = (1, 0)\) along the x-axis:

- \(u \cdot (1, 1) = 1\) → acute angle

- \(u \cdot (0, 1) = 0\) → right angle

- \(u \cdot (-1, 0) = -1\) → opposite

price and bedrooms both trend up → large positive \(y^T x\)

orthogonality = best fit

the best prediction makes the residual orthogonal to every feature:

\[\mathbf{1}^T \epsilon = 0 \qquad \text{and} \qquad x^T \epsilon = 0\]

- first: residuals sum to zero (same as the mean model!)

- second: residuals have no remaining linear pattern with \(x\)

if some feature still aligned with the residual, you could reduce error by adjusting its coefficient

normal equations

Normal equations (simple regression)

\(\mathbf{1}^T \epsilon = 0 \quad \text{and} \quad x^T \epsilon = 0\)

where \(\epsilon = y - \beta_0 \mathbf{1} - \beta_1 x\)

the algebraic form of “residual orthogonal to features”

these two equations determine the unique \((\widehat{\beta}_0, \widehat{\beta}_1)\)

the projection picture

![]()

\(\widehat{y}\) = orthogonal projection of \(y\) onto \(\text{span}\{\mathbf{1}, x\}\)

the right angle is why it’s the best fit

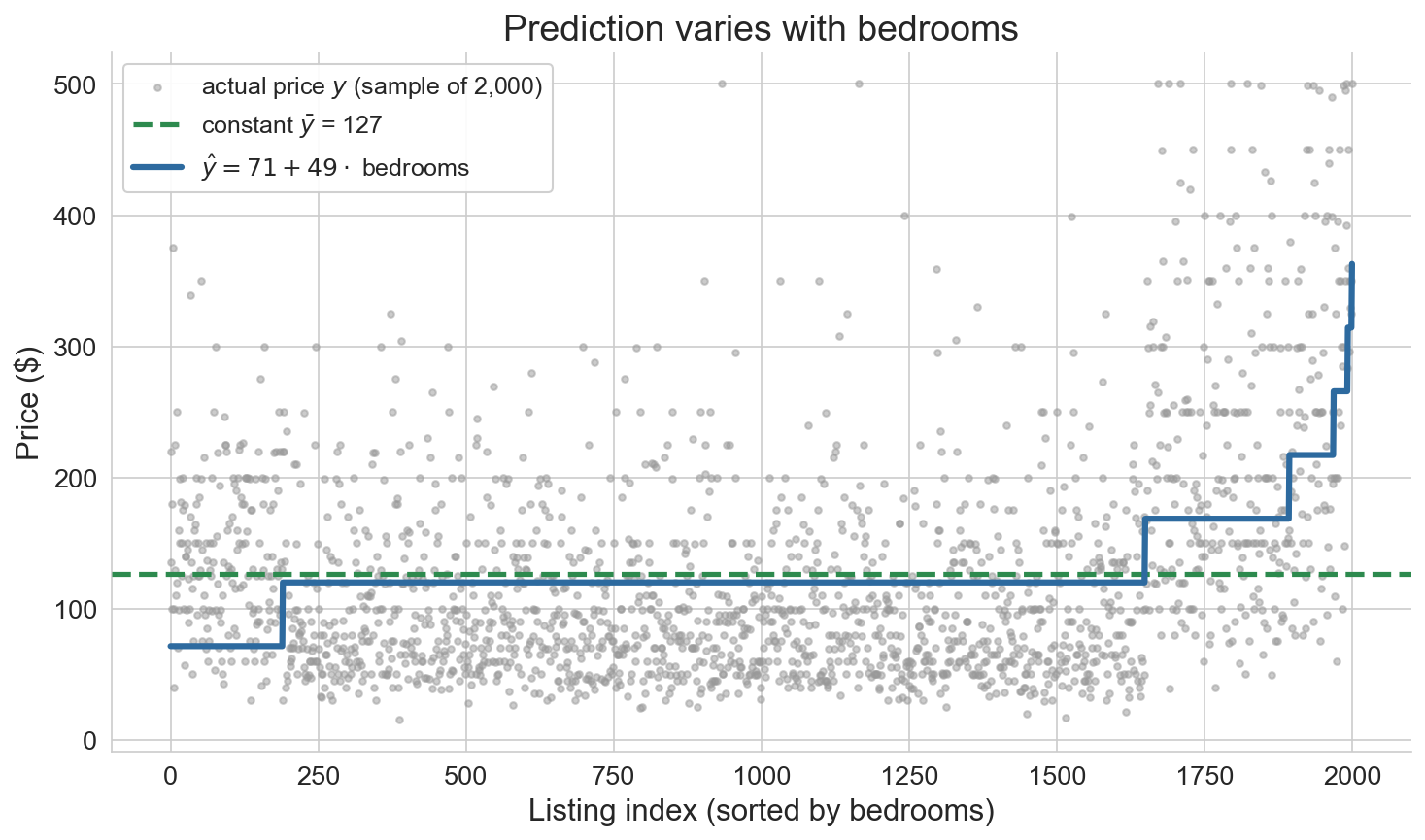

simple regression on Airbnb

model = LinearRegression()

model.fit(df[['bedrooms']], prices)

ŷ = 71 + 49 × bedrooms

R² = 0.156

\[\widehat{y} = 71 + 49 \times \text{bedrooms}\]

interpreting the coefficients

\[\widehat{y} = 71 + 49 \times \text{bedrooms}\]

- intercept $71: predicted price for a studio (0 bedrooms)

- slope $49: each additional bedroom → $49 more per night

association, not causation: larger listings differ in many ways

plug in a few listings

\[\widehat{y} = 71 + 49 \times \text{bedrooms}\]

| studio |

$71 |

| 1-bedroom |

$120 |

| 3-bedroom |

$217 |

| 5-bedroom |

$314 |

back to our friend’s 2-BR: model predicts $169/night

verify orthogonality

y_hat = model.predict(df[['bedrooms']])

residuals = prices - y_hat

np.dot(residuals, np.ones(len(df))) # ≈ 0

np.dot(residuals, df['bedrooms'].values) # ≈ 0

residuals · 1 : -0.0000 ✓

residuals · bedrooms: -0.0000 ✓

the errors have no linear pattern left that bedrooms could capture

what would a curved pattern in the residual plot mean?

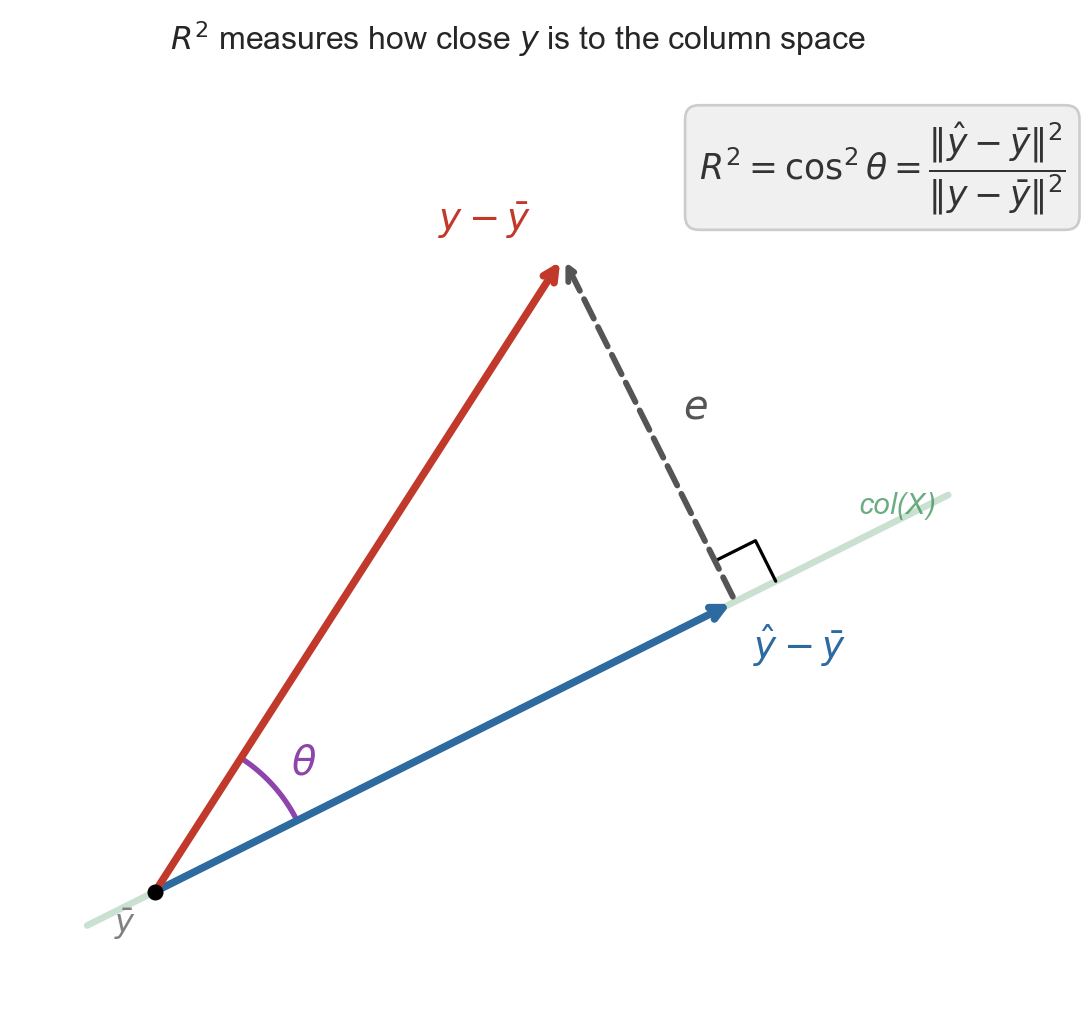

\(R^2\): fraction of variance explained

\(R^2\) (coefficient of determination)

\[R^2 = 1 - \frac{\|\epsilon\|^2}{\|y - \bar{y}\|^2}\]

- \(R^2 = 0\): no better than predicting \(\bar{y}\)

- \(R^2 = 1\): perfect fit

for our Airbnb regression: \(R^2 = 0.156\)

correlation

Correlation (Pearson’s \(r\))

\(r(u, v) = \dfrac{(u - \bar u)^T(v - \bar v)}{\|u - \bar u\|\,\|v - \bar v\|}\)

inner product of centered, length-normalized vectors.

- \(-1 \le r \le +1\)

- \(r = 0\) → centered vectors are orthogonal

- unitless: rescaling \(u\) or \(v\) doesn’t change \(r\)

\(R^2 = r(y, \widehat{y})^2\)

![]()

Pythagorean theorem (centered \(y\)):

\[\|y - \bar{y}\|^2 = \|\widehat{y} - \bar{y}\|^2 + \|\epsilon\|^2\]

\[R^2 = \frac{\|\widehat{y} - \bar{y}\|^2}{\|y - \bar{y}\|^2} = r(y, \widehat y)^2\]

the first ratio is the correlation between \(y\) and \(\widehat{y}\), by definition

\(R^2 = r^2\) in simple regression

r = df['price'].corr(df['bedrooms'])

# r = 0.3944

model.score(df[['bedrooms']], prices)

# R² = 0.1556 = r²

for one predictor: \(R^2\) is literally \(r\) squared

(with multiple predictors, only \(R^2\) applies)

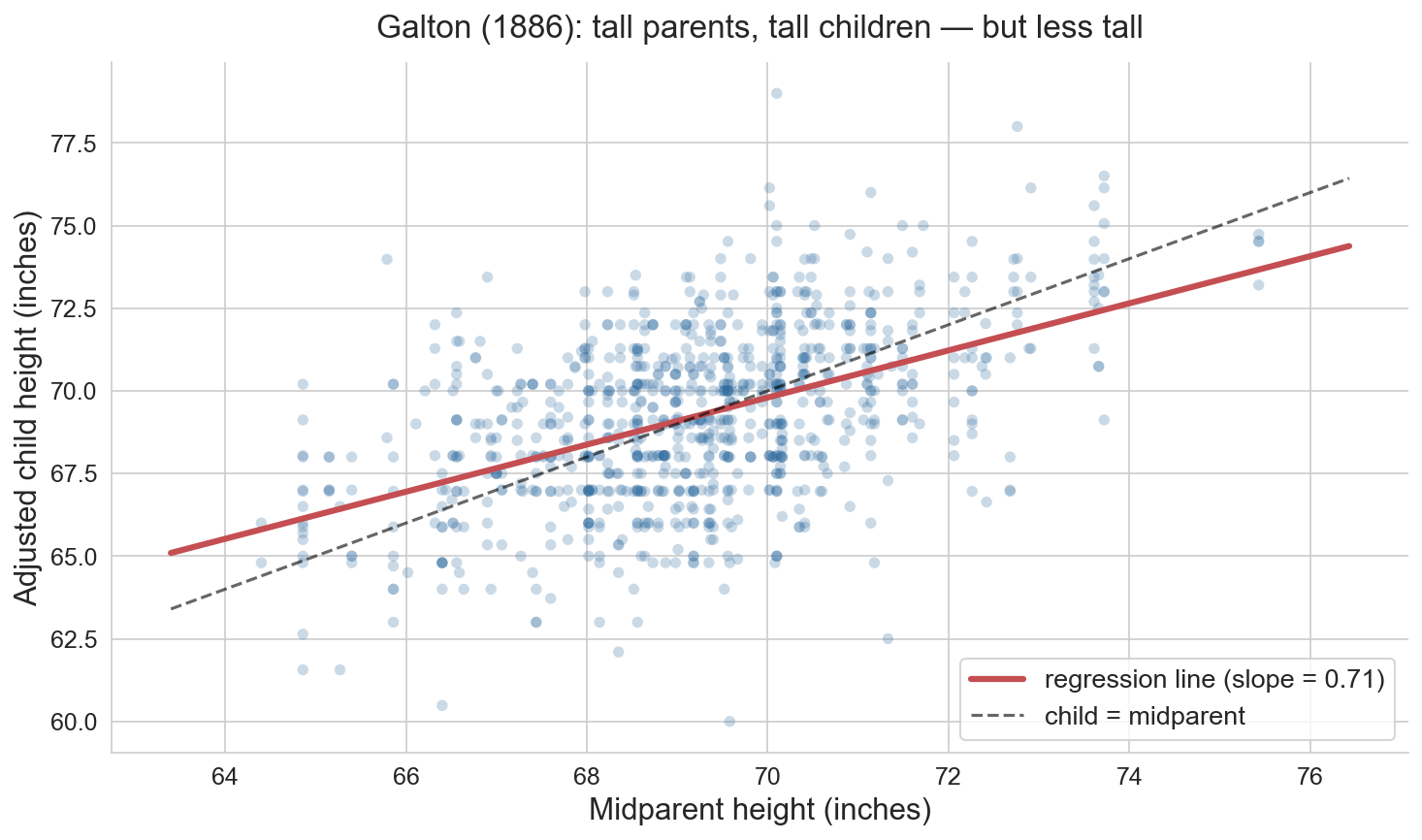

Galton’s heights

Francis Galton, 1886: tall parents → tall children, but less tall

934 children, 205 families: \(r \approx 0.50\), slope \(\approx 0.71\) (Galton’s own estimate: 2/3)

why “regression”?

since \(|r| < 1\), predicted \(y\) is always closer to \(\bar{y}\) (in SDs) than \(x\) is to \(\bar{x}\)

Galton called this “regression toward mediocrity”. the name stuck

purely statistical, not biological or causal

where else do you see regression to the mean?

- a team wins 90% of games one season. next year?

- a student scores in the 99th percentile. next exam?

- a player scores 45 points (season avg: 25). next game?

why does this keep happening?

skill + luck, luck resets

90% win rate = part skill, part luck

next season: the skill carries over, the luck resets

99th percentile exam = real knowledge + a run of favorable questions

knowledge holds; favorable run does not

whenever \(|r| < 1\), extremes on one measurement look less extreme on the next

key takeaways

- two views of data: rows = points, columns = vectors in \(\mathbb{R}^n\)

- the mean is the best constant predictor under squared error

- simple regression is the orthogonal projection of \(y\) onto \(\text{span}\{\mathbf{1}, x\}\)

- residual ⊥ features: the defining property of least squares

- \(R^2 = r(y, \widehat{y})^2\): how much of \(y\) lives in the feature span

- regression to the mean: extremes don’t persist

what we can’t answer yet

\[\widehat{y} = 71 + 49 \times \text{bedrooms} \qquad R^2 = 0.16\]

- what about bathrooms? room type? neighborhood?

- can more features make \(R^2\) bigger?

- how do we encode categorical features?

next time: multiple regression (Chapter 5)

logistics

- read Chapter 4 before next lecture

- HW 1 due Friday April 10

- quiz 2 next Wednesday: covers Lec 4–5

one-minute feedback

- what was the most useful thing you learned today?

- what was the most confusing?

give feedback